As many agents and brokers may attest to, the obtaining of updated insurance information for applications can, more often than not, be time-consuming, labor-intensive and just plain inefficient.

Enter Broker Buddha. With a promising name and and equally inspiring purpose, this new New York-based insurtech is aiming to bring nothing less than harmony and enlightenment to the commercial insurance sector. With its creation of insurance “smart forms” accessed via its online platform, Broker Buddha has made obsolete the laborious process of agents and brokers filling out and emailing (or even still faxing) .pdfs of new or renewal policy forms to their insureds.

The premise is simple. Let technology help brokers do what they do best, while Broker Buddha does the rest. Read on to learn more in our latest Agency Interview:

Thank you for taking the time to discuss Broker Buddha with Agency Checklists

I am happy to have the opportunity to showcase where Broker Buddha can help the independent agency compete in today’s rapidly changing marketplace.

Where exactly did the name “Broker Buddha” come from and what does it signify?

Where exactly did the name “Broker Buddha” come from and what does it signify?

As an entirely new company, we wanted our name to imply something about our target customer and the value we provide to them. We also wanted the name to be memorable.

I think we nailed it with “Broker Buddha” because our target customer is stated in our name, and the reference to Buddha/Buddhism carries a meaningful implication about our value. The alliteration in the name makes it memorable as does that slightly abnormal reference to something religious in the workplace.

What is the short summary of what Broker Buddha’s sees as its mission?

Everybody knows that having insurance is important, but the experience of buying and selling insurance today is pretty painful especially commercial insurance. I have spent ten years of my career building technologies for large enterprises that help drive revenue and reduce costs. I know how to spot an opportunity, and I know how to build solutions to capitalize on it. I have also spent ten years of my career building consumer-mobile products in music, fitness, and social media, so I know that people’s eyes light up when they see a beautifully-designed product with high-resolution images and dynamic animations.

We started Broker Buddha because we identified a huge opportunity to bring technology to brokers, and give them something that they have been waiting for since the Internet showed up twenty years ago. And so far we have the only platform which actually makes them excited to use technology to impress their clients. So, we give them, and their clients, a beautifully-designed, intuitive online experience, which takes the pain out of buying and selling insurance, and the result is a platform which increases retention and close rates, while also saving them time.

What does this solution mean operationally for brokers or agents who use it?

The solution is a cloud-based software platform to put applications and renewals into an interactive, customer-friendly online experience.

The process of collecting application information from clients today is typically pretty painful. It is either done over the phone, in person, using PDF, paper, sometimes fax machines and email. It is inefficient, and it is time-consuming. We created a solution which automates that process for brokers, in a way that makes them feel proud to use technology with their clients.

You spoke about having spent a decade building technologies for large enterprises. Could you expand on that and give us some of your background and how you became involved with Broker Buddha?

I grew up in New Orleans, but moved to Boston and went to college here at Harvard where I got a degree in computer science. After college, I spent the first half of my career working for large corporations, like Accenture and Nextel. For the second half of my career, my work has been with startups and has included running business development both at Shazam and Tumblr. In between, I also founded a few of my own startups.

During my time developing startups, I met a guy named Mark Peter Davis. Mark was the managing director of a company called Interplay Ventures. Interplay both invests in and starts companies.

One of the companies started with Interplay’s involvement is a company called Founder Shield. Founder Shield is one of the fastest growing insurance brokerages in the country, primarily because they use technology to engage with their clients.

About a year ago, I reached out to Mark because I was looking to get back into the startup world, and asked him, “Do you have anything interesting for me?” And he said, “Look, we have this company that we’ve just created, based on the technology that powers the Founder Shield insurance brokerage business, and we need a CEO to run it.”

He said they wanted somebody with technology and sales experience, and it did not bother them that I had not been in the insurance industry before. They felt like it was something I could learn quickly. So we had a couple of meetings. I talked to my brother, who is an insurance broker in California, and I asked him, “Look, I do not know much about this industry, but these guys are telling me that people are still using pretty antiquated tools.” And he said, “Yeah if you guys can solve that problem, it’s a big business.”

So, a year later, here I am with that startup, Broker Buddha.

How long did it take you to develop the Broker Buddha product to a point where you thought it was ready?

I joined in March of 2017 and inherited the technology that was built for Founder Shield originally. The first part of my responsibilities was to take that technology, that was built for one insurance broker, and turn it into a platform that could be used and configured for any insurance brokerage. Ultimately, we spent about six months doing that technology conversion, and officially launching the product in October of 2017. Since our launch, we have been doubling users every month.[pullquote]The entire platform is branded for the agency…There is no “Broker Buddha” branding on the platform anywhere.[/pullquote]

What was the target market you aimed to serve and is the actual market that has responded the same market you originally thought would use Broker Buddha?

We started out with a pretty broad assumption that this would apply to any independent agency, which is obviously a very broad market. We did not know if it would be better for small, medium, or large agencies. And so far, we have small clients, we have medium-sized clients, we have large clients, and they all benefit from it.

For example, there is a company, recently acquired by HUB, who uses it, there is a team at Lockton who is going to start using it, and we also have a lot of small and medium-sized agencies on the platform. So, the answer is, it seems to work for all types of independent agents thus far.

There is a different way of looking at the market, though. Instead of thinking about company size, one should consider the generation of the leaders in the brokerage. It is probably not surprising, for example, to hear that younger agents are more comfortable making quick decisions to adopt the technology. And in particular, when we find family agencies with an up-and-coming leader, usually the child of an owner stepping into leadership roles in the business, that is really where we have seen a lot of excitement about our product.

Also, we were pleasantly surprised because that there even seems to be an opportunity for captive agencies, which is not a group that we originally intended to engage with. They sometimes write independent business when their own company cannot handle it. When this happens, they end up having the same problem that independent brokers do, which is that they do not have any tools to collect information from clients.

About the generational gap in agencies, we have heard about this issue of not embracing technology, in particular agents who have trouble adapting to new methods and technology. Streamlining the application process, however, seems like something that can be easily understood and embraced by a lot of different types of agencies, as you said.

No question. The only difference is, younger agents expect these tools to exist, and are very frustrated that they do not. And when they hear about us, they are quick to adopt it. Older agents have not necessarily conceived of this in their minds, but when they do see it, they are impressed and interested, but it might take a week or two to get them over the line, whereas a younger person’s like, “Man, I have been waiting for this my whole life.”

What is Broker Buddha’s geographic distribution so far? Can you operate in all 50 states, or do you have any restrictions?

Not that I know. We do not sell insurance. We provide a software platform for people who do. We have signed up brokers in California, New York, we have got brokers in Florida, Alabama, Texas, Georgia, New Jersey, New York. We also just signed our first client in Boston.

How is Broker Buddha’s pricing? Do you have variations in pricing based on the size or type of agency?

Yes, while we have single-user pricing, we do volume discounts as you get bigger, and then we do full agency pricing based on how many people they expect to use it. We are flexible. For example, we’ll put together a pricing package based on how many power users you have, and then how many casual users you have.

On renewal applications, how does that work?

One of the things that we recognized very quickly was that an established broker makes the majority of their money from their renewal business. They did the hard work of getting that business, and they have built up their nice book, and their job is to renew as close to 100% of that as they can every year. Now, with some of those policies, you can just auto-renew directly with the carrier. There’s nothing needed. But increasingly carriers want a signed, completed applications every year.

The challenge in the process of getting a signed application back involves either asking the client to fill out a form again, or as a broker, pre-filling the applications, and then sending them out to the client. After that, it is then nagging the client to fill out and send back the forms, and then nagging the client, and nagging the client, until finally getting it back, usually two days before the policy is due.

In response, we at Broker Buddha have built our platform and an operations team to essentially manage that process, and we can do it way more efficiently than anybody else because we have got the systems to do it.

Could walk through for our readers how Broker Buddha works in practice? For a new broker signing up, what are you going to tell me that they are going to do differently and then if that broker is signing up a new client how is the application process going be different for that potential client?

We designed our product to map exactly to the way a broker currently operates. Regardless, we provide white glove user onboarding and support throughout. For every new user, we schedule a one hour kickoff and training call with your account manager where we will walk you through all the key features of the platform, and train you on how to use them. After that, we do weekly follow-up calls with you and your team until you feel fully ramped up.

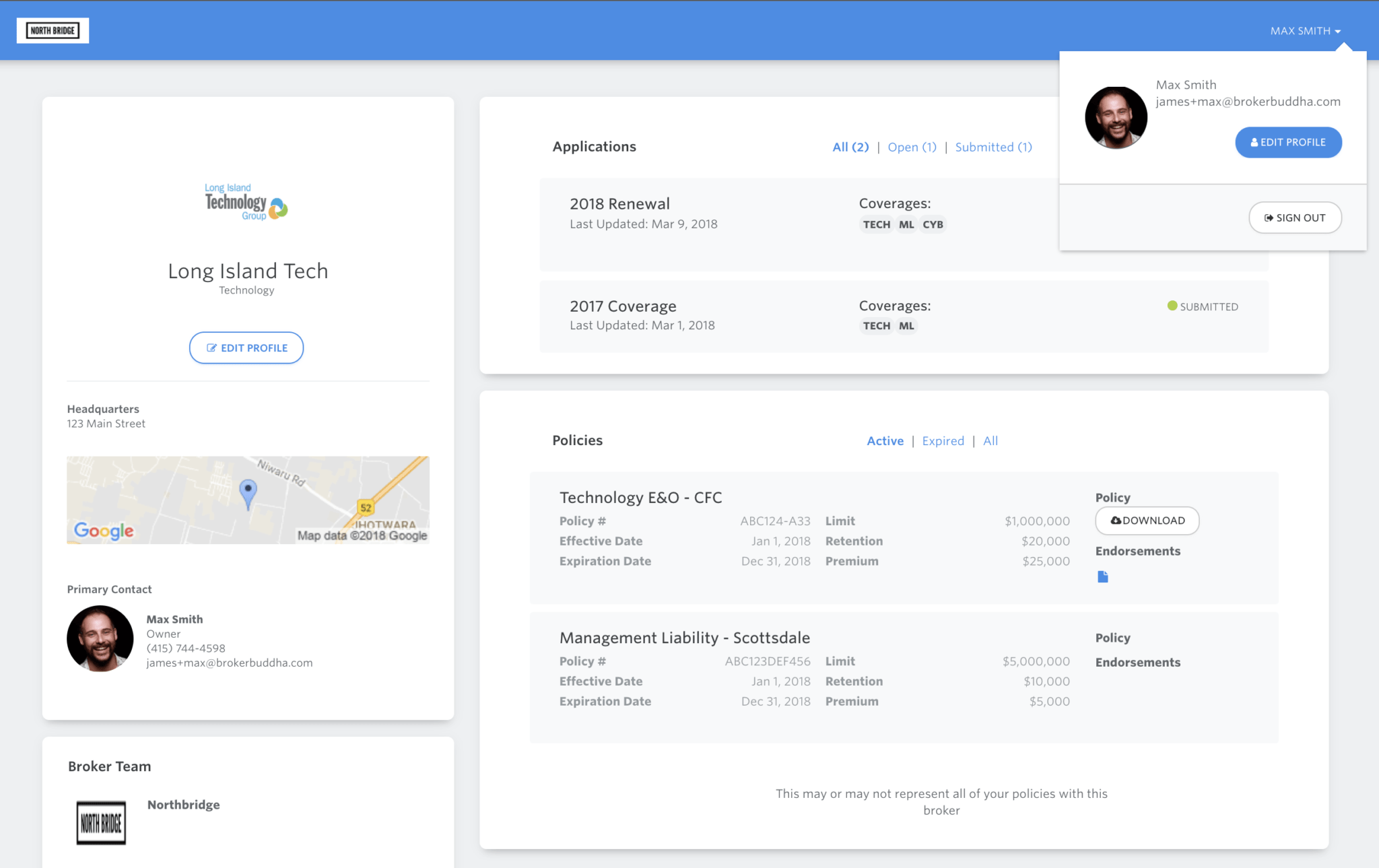

There are three key uses of the platform. The first is renewing a policy. For that use case your account manager will onboard all of your prior year data, putting it onto the platform, and when you are ready to send out your renewal applications, you just click a button that says renew, and it generates a copy of all the data, which you can then send to your clients through our platform.

Number two is, you can create a link in our system that you can put on your website, so a client can come to your website and start the application process themselves. That is something that more tech-focused people are doing.

The third scenario maps to the way most brokers handle new business. After you meet with your client and learn about their business, you would normally go back to the office, fill out some forms and then email them to the client to complete and sign. With Broker Buddha, you simply log in to our platform, create an application for that client, you select the forms that you need, and you input all of the client’s information online. Any information that is common across the forms is mapped so that you only have to enter that information once. Once you have finished inputting as much as you can, you send a link to the client to answer the remaining questions. In turn, the client, instead of receiving an email with three attachments, receives a link to a webpage. After clicking the link to the webpage, which is interactive, the client is guided through the rest of the application process with helpful hints and tips along the way. It tells them which questions are required, and it only asks them the questions that are relevant.

The goal is to avoid the doctor’s office-like experience of filling out seven different forms with the same basic questions on every different form.

In the third case, if a prospective or present insured of the agency gets a Broker Buddha link to complete an application, do they know they are going to Broker Buddha, or does the website appear as an agency portal?

The entire platform is branded for the agency. You control all of the images, all the logos, as well as which forms the client can fill out. There is no “Broker Buddha” branding on the platform anywhere.

What protection is there for the agency expiration information? As you know, that is an agents prime asset, so how is it protected by Broker Buddha?

We put agreements in place with both the broker and their clients. When a client logs on, they agree to our terms of service, and those terms of service state that they own their data, so anything the client submits, is owned by the client.

When I worked at Tumblr, I recognized the significance of user content rights and brought that learning with me to Broker Buddha. Standard practice is that the user owns the things they post, but they give the platform a license to use it for specific purposes. So, they give the brokers a license to use it to get their insurance, and they give us a license to use it to operate the platform. Legally, we are not allowed to use it for any other reason. And if we did, no broker would ever work with us again.

Regarding insurance companies, how do you work with them?

Today, the platform is exclusively built to facilitate the relationship between the broker and the insured, to collect information to put on an application. Once the broker has the application, they do whatever they used to do before. So, if they put that into an agency portal, they would do that. If they emailed the application to an underwriter to get a quote, they do that. So, that is what is happening today.

We are in talks with a number of underwriters about integrations to digitally enable the end to end submission process. We also signed a partnership with a major wholesaler who will be giving our platform to several thousand of their retail brokers because they want to use it as a better way to engage with them digitally.

How many people work on the Broker Buddha team?

As of today, we are a team of ten. We have a mix of account managers, developers, [as well as] a foreign production team.

On your site, it mentions a mobile app for Broker Buddha. Is that something that is offered to the agent, or to the insureds, or both?

We do not have a mobile app today, but we do support mobile form filling and eSignature. We allow clients to complete and sign applications on their phone. When a broker is ready for a client to submit an application, they send them a link in their email. The client clicks on that link, it will open a browser, and they can complete that application there.

And that is branded to the agency, too?

It is.

Since you have started your new career in the insurance industry, have you any new insights or trends that you have seen and would like to share?

Well, I can tell you personally … talking about insurance at a cocktail party is usually a conversation killer, right? And with all due respect to everybody who is in it, it is a great business, but it is just not that sexy, especially commercial insurance. Unless you are a chief financial officer or a general counsel, it is not really something you know about or talk about. Having spent the last ten years working for popular consumer-mobile brands like Shazam and Tumblr, I knew that would be an adjustment for me.[pullquote]From an opportunity perspective, I can tell you that all the things that I was told before I joined, about the number of inefficiencies in the industry, and the opportunity to make an impact, is 100% true.[/pullquote]

But, what I found is that people in the industry are some of the most entertaining people to know and be around. Maybe, it is just because brokers are naturally good salespeople and personable, but I have found the people in this industry to be very warm, and kind, and fun. It has been a really enjoyable transition for me, from a personal perspective.

From an opportunity perspective, I can tell you that all the things that I was told before I joined, about the number of inefficiencies in the industry, and the opportunity to make an impact, is 100% true. And that has been validated by all the conversations we have had with brokers who, when we tell them what we are doing, they are just like, “Yeah, this would save me a lot of time.” So, in that respect, it has been really rewarding.

Do you see anybody else doing what you are doing out there with improving the application interface?

There are people who are trying to imitate us, but nobody who compares. Where we have differentiated ourselves is our focus on making brokers excited to use technology to impress their clients. Other products we have seen are functional and solve similar back-office efficiency problems, but nobody has created a tool which inspires brokers to use technology as a way to engage with their clients.

Do you see Insurtech as it goes forward as focusing more on the improvement of the existing agency system, as opposed to attempting to create direct marketing channels?

I think what people are starting to recognize is how big an industry insurance is. Early on, people were saying, “Oh yeah, brokers will be replaced by technology.” And people thought the whole industry would be replaced by technology, which was a very uneducated assumption, and, I think, a function of the fact that not a lot of people know a lot about the industry.

What we have seen is that in certain pockets like personal lines, health, and benefits, even micro-commercial, where people are spending $1,000 on an insurance policy, there are some great products out there, which I think can be an alternative to brokers.

When it comes to selling commercial insurance, though, if somebody’s spending $10,000 on their commercial insurance for their business, those people are not going to buy from a computer. There is no way. And so there are now technologies and Insurtech companies who are coming along to enable those brokers. So, it is not an either-or, and it is just a question of where you fit in.

How is Broker Buddha funded?

Thankfully, we have not needed to raise much money. People are willing to pay for the product which funds most of our operations. Some of our clients like the product so much that they have made capital investments themselves. On the whole, we are very capital efficient. As part of Interplay, we get a lot of support around best practices, access to talent, and access to other companies in the network who provide services for us.

One of the other questions I had was the relationship between Broker Buddha and Founder Shield. Are they affiliates, or are they entirely independent?

They are two separate companies. The product was originally built specifically for them by contractors at Founder Shield’s direction; Founder Shield basically guided the development of that. From there, Mark at Interplay recognized that this was a huge potential stand-alone business and hired me to run it.

What kind of contractual provisions do you have with your agency users?

All of our brokers and users have to agree to our terms of service.

What has been your biggest challenge and what has been the biggest success since you started this?

I think I underestimated the amount of work it would take to convert the original platform into a fully cloud-based platform. I thought that would be a short project. It took probably twice as long as I expected. I have been in tech for twenty years, and I should have known better.

We quickly learned that supplemental applications are an area of the broker operations for which there is no other solution besides email and PDF. So, we got very specific from a product perspective around just solving that one problem, and doing it in a way that would allow brokers to impress their clients. And that has been a huge success. From there, the investment in the design and the graphics, and the animations have really been important. We have heard back from our clients that they love that.

You mentioned supplemental applications. Could you just expand on what you mean by that?

Sure. This was another one of those new things for me when I came in from the outside; an application was an application. But what I learned was, in insurance there is really two categories of applications. You have ACORD forms, which are sort of like common apps, if you will, for any different policy, and pretty much every carrier will expect them.

In addition to those, however, you also frequently have these things called supplemental applications, which are specific to each carrier, and each product line. There is this vast library of PDF forms out there, which brokers have to send their clients to get them completed.

Now, those are typically used for specialty lines, excess lines, surplus lines, things that are pretty non-standard. But, carriers are expecting them more and more, and brokers are using them more and more. So really focusing on a solution around those has been great for us.

You obviously are dealing with a lot of data with respect to insureds and their personal information. Do you have cyber coverage in case you have a data breach?

We have cyber coverage, which from a security perspective, our head of security used to be the chief technical officer for a health tech company, so we are buttoned up there. All of our data is encrypted both in transit and while it is stored in our database.

How do agents, and others, find out more about more about Broker Buddha?

They can start on our website: www.brokerbuddha.com where they can also book a demo. [In addition, interested agents or brokers] also can call me directly if they want to at 415-744-4598.

Thank you so much for taking the time to tell our readers and us about Broker Buddha.

It was my pleasure. Thanks for the opportunity and the support.