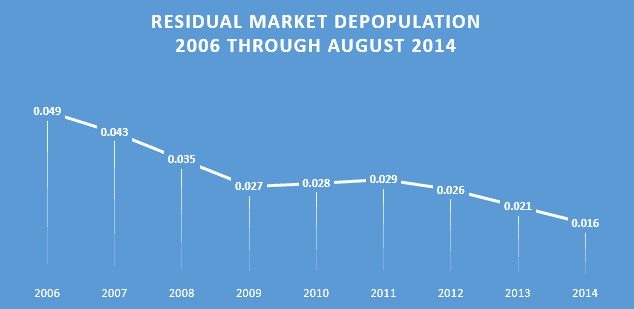

A 2009 report of the Division of Insurance stated that “One of the fundamental goals of managed competition” was to have “a small residual market.” Data provided by Commonwealth Automobile Reinsurers (CAR) evidences that the Division seems to be getting its wish. The chart below shows that as the Massachusetts insurance industry began to prepare for managed competition and the advent of an assigned risk system to be implemented on April 1, 2008 the residual market began to shrink from just under 5% of the automobile insurance market to a just a little more than 1.6% of the projected market for 2014.

This chart actually shows the tail end of a twenty-five year process of depopulation of the residual automobile insurance market that began in 1988.

The residual market has declined from a one time high of 70% of the personal automobile insurance market to less the 2% today

Depopulation of the residual market became a major political in issue in the late 1980s. The residual market plan established in 1983 for motor vehicle insurance provided for the assignment of each licensed property and casualty insurance producer a Servicing Carrier. This unique in the nation system of assigning agents rather than insurers to a servicing carrier coupled with automobile insurance rates being fixed and established by the Commissioner of insurance annually quickly resulted in a ballooning of the residual market. By 1988, the residual market totaled an amazing 70% of the total market for automobile insurance in Massachusetts. That year the legislature enacted a reform package to start the process of depopulating the residual market and reducing the number of agents who only had a market for automobile insurance through their CAR assigned servicing carrier. However, the real impetus for a major change to the then existing system came on the last day of 2004, when the commissioner ordered the assigned agent plan phased out by January 1, 2008, to be replaced by an assigned risk plan. An appeal by companies opposed the change to an assigned risk plan to the Supreme Judicial Court failed in 2006, and the assigned risk plan and competive rating began on April 1, 2008.

Assigned risk numbers overall continue to decline

Besides the decline in the overall percentage of the Massachusetts automobile insurance market that makes up the residual market, there is a corresponding drop in the absolute number of assigned risks exposures. Over the course of managed competition the number of assignments has also declined as evidenced by the following chart.

This decline in the absolute number of assigned risk exposures has been coupled with a general increase in the number of overall exposures in the marketplace over a similar period of time. The total automobile insurance market exposures have increased 10% between 2009 and 2013.