The annual Insurance Regulation Report Card is now in its fifth edition

[pullquote]We commend the department for running a lean budget, but it remains the case that Massachusetts is a very expensive state in which to do business – R.J. Lehmann[/pullquote]

The insurance marketplace continues to be one of the largest and most significant segments of the financial services industry sectors that is still almost entirely regulated at the state level. Since 2012, the R Street Institute, a non-profit, non-partisan public policy research organization, has taken on the job of examining each of the 50 states to determine which ones do the best job in regulating the “business of insurance.” The results then are published in R Street’s annual Insurance Regulation Report Card.

Now in its fifth edition, the Insurance Regulation Report Card “grades” each state, via seven different dimensions, to determine how effective and efficient each state is in the discharge of their duties with respect to insurance.

The underlying belief behind the Insurance Regulation Report Card, is to determine which state regulatory systems best embody the principles of a limited and efficient government. As R Street Senior Fellow, Editor-in-Chief and Co-Founder, R.J. Lehmann, states:

“We believe states should regulate only those market activities where government is best-positioned to act; that they should do so competently and with measurable results; and that their activities should lay the minimum possible financial burden on policyholders, companies and, ultimately, taxpayers.”

Mr. Lehmann cautions, however, in this edition, as he has cautioned in past editions, the report card should not be seen as an indictment against certain states or their commissioners:

“…The organization emphasizes that the report is not intended as a referendum on a specific regulator but rather “… our best attempt at an objective evaluation of the regulatory environments in each of the 50 states.”

To achieve that goal, the R Street Institute asks the following three basic questions in analyzing a state’s regulation of its insurance industry:

- How free are consumers to choose the insurance products they want?

- How free are insurers to provide the insurance products consumers want?

- How effectively are states discharging their duties to monitor insurer solvency, police fraud and consumer abuse and foster competitive, private insurance markets?

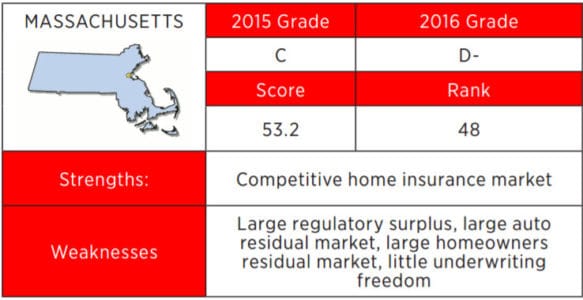

Massachusetts falls back to the bottom of the barrel this year

While our neighbor to the North, Vermont, once again received top marks in 2016, Massachusetts actually got a worse grade in 2016 than it did for 2015. In 2013, the Commonwealth received a “C-“, then dropped to a “D” in 2014, but rallied in 2015, when the Bay State’s grade improved to a solid “C”. The improvement was short-lived, however, as Massachusetts barely earned a passing grade this year with a “D-“.

As noted in a screenshot of Massachusetts’ 2016 Report Card, while R Street highlighted the state’s competitive home insurance market as a strength, the Commonwealth was marked down for various factors including large auto and homeowner’s residual markets and little underwriting freedom.

More about the R Street’s Massachusetts Grade

As anyone who has gone to school would agree, it is sometimes hard to know why you are given a certain grade, but the best way to improve is often to ask why you were graded the way you were.

To that end, we queried Mr. Lehmann on his views as to why Massachusetts garnered such a low grade for its overall performance. Here is what he wrote us:

The area where the state continues to be the greatest outlier is in the ratio of the regulatory fees it charges to insurance companies and insurance agents, compared to the amount it actually spends on regulation.

In 2015, Massachusetts Insurance Department $14.1 million on regulating the business of insurance, but it collected more than eight times that amount, $130.7 million, in regulatory fees and assessments from the insurance industry. That does not include the $325,421 in fines and penalties insurance companies paid the state, much less the $362.16 million in premium taxes that were paid by insurance consumers.

We commend the department for running a lean budget, but it remains the case that Massachusetts is a very expensive state in which to do business. Bringing down these fees to make them at least roughly resemble the actual cost of regulation would encourage more firms to begin writing business and reduce the impact of this stealth tax on the cost of insurance.

The other major area of concern is the lack of underwriting freedom in the state and how that serves to create relatively large residual markets. The “managed competition” initiative has made great strides in shrinking the size of Commonwealth Automobile Reinsurers, which now accounts for just 1.4 percent of the market, when it was as high as 70 percent 30 years ago. It should be noted, however, that it remains the third largest residual auto insurance market in the country, behind only North Carolina and Rhode Island.

There’s also been some progress on the property insurance side, where the Massachusetts Property Insurance Underwriting Association has declined from about 7.3 percent of the market in 2011 to 6.5 percent of the market as of 2015. But because most other residual property insurance markets have been shrinking much faster in the prevailing soft property insurance cycle, the MPIUA is now the single largest residual property entity in the United States, larger even than Florida Citizens.

Governor Charlie Baker and Insurance Commissioner Daniel Judson have made clear that they are interested in removing burdensome regulations that hinder the Massachusetts economy. If they could find ways to reduce excess regulatory fees and extend more underwriting freedom, we expect the state could improve its report card score drastically.

The Top 10 best states for insurance regulation according to R Street

With those thoughts in mind, here are the ten states this year that R Street says are doing it right:

-

Vermont “A+”

-

Utah “A”

-

Maine “A”

-

Illinois “A”

-

Idaho “A”

-

Arizona “A”

-

Wisconsin “A-“

-

New Hampshire “A-“

-

Kentucky “A-“

-

Nevada “B+”

And the top ten who make up the other end of the list…

On the other end of the list, these ten states were given the lowest marks for their regulation of insurance. While Massachusetts is not the worst, it’s close.

-

New York “D”

-

North Dakota “D+”

-

Montana “D”

-

Delaware “D”

-

Mississippi “D”

-

Louisiana “D”

-

Hawaii “D”

-

California “D”

-

Massachusetts “D-“

-

Arkansas “D-“

-

North Carolina “F”

For those interested in taking a look at the official report, a copy can be accessed by clicking the link below:

View the R Street’s 2016 Insurance Regulation Report Card here