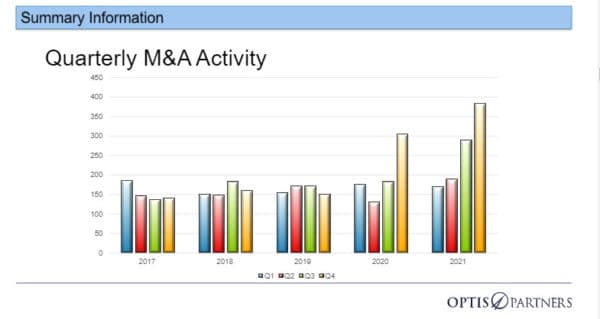

The numbers are in and there is no doubt: insurance agency mergers & acquisitions for the year 2021 has ‘blasted past’ all expectations. According to the latest data from OPTIS Partners’ quarterly report there were 1,034 announced insurance agency mergers and acquisitions in 2021. This number is up 30% from the 795 transactions reported in 2020.

“If 2020 was a boom year for mergers and acquisitions, 2021 was a virtual explosion,” said Steve Germundson, partner at OPTIS Partners.“The fourth quarter rush to close deals by year-end clearly taxed the sellers’ deal teams, legal counsel, and due-diligence providers. We expect a bit of a first-quarter respite before the cycle picks up again.”

As for the fourth quarter of 2021 (Q4-2021), there were 384 deals announced representing a 26% increase over the same time period during 2020 and a 68% increase over the same quarter in 2019. This number was also 32% more than the 290 transactions reported for Q3-2021, as sellers once again looked to avoid a potential tax increase.

According to OPTIS Partners the sustained rate of acquisitions continues due to investors flush with capital meeting an increasing supply of business owners looking to take advantage of all-time high valuations while capital-gains tax rates are low.

OPTIS Partners data covers U.S. and Canadian agencies selling primarily property-and-casualty insurance, agencies selling both P&C and employee benefits, and those selling only employee benefits.

How the OPTIS Partner Quarterly Report compiles its data

The quarterly OPTIS Partner report includes data covering both U.S. and Canadian agencies ‘selling primarily property-and-casualty insurance, agencies selling both P&C and employee benefits, and those selling only employee benefits.’ It breaks down buyers into four distinct groups:

- private equity-backed/hybrid brokers,

- privately held brokers,

- publicly held brokers, and

- all others

Sellers are categorized as follows:

- property & casualty brokers,

- property & casualty and employee benefits brokers,

- employee benefits brokers, and

- all others

Private equity/hybrid groups continue to buy up the majority of agencies

Private equity/hybrid group money continues to dominate the insurance agency mergers and acquisition market representing approximately 76% of all transaction. In comparison, acquisitions by privately held firms and publicly traded companies decreased to 15% and 6% of all deals, respectively.

The most active privately-owned buyers in 2021 were Heffernan Insurance Brokers with 11 transactions (up from 8 in 2020) and Liberty Company Insurance Brokers with 10 deals completed (up from 1).

Acrisure is again the top agency buyer of 2021

As it has been throughout 2021, Acrisure was the leading agency buyer in 2021 with a total of 122 transactions, 17% higher than their five-year average.

While it remained at the top spot, OPITS noted that for the first time in many years, another buyer competed for the top spot. In second place was PCF Insurance with 99 completed transactions (up from 36 in 2020). Other top buyers were Hub International with 61 acquisitions (down from 65 in 2020) and High Street Partners with 56 (up from 9 in 2020). Both PCF and High Street recapitalized in 2021. Assured Partners with 51 deals (up from 38 in 2020) rounded out the top five.

Other buyers considered “most active” included World Insurance Associates with 49 (up from 42) and both Alera Group and BroadStreet Partners with 45 (up from 18 and down from 58, respectively). OPTIS Partners also noted that Baldwin Risk Partners also was one of the most active acquirers of top 100 firms by size. In late 2021, the company made its first foray into New England with its purchase of RogersGray.

Several other historically active buyers saw their transaction count drop somewhat in 2021, including Hub and Broadstreet, noted above, and OneDigital at 20 compared to 32 in 2020.

The following chart reproduced from the report, highlights the buyers with 20 or more deals in 2021

| Buyer | 2017 | 2018 | 2019 | 2020 | 2021 |

|---|---|---|---|---|---|

| Acrisure | 92 | 101 | 98 | 108 | 122 |

| PCF Insurance | 4 | 4 | 36 | 99 | |

| Hub International | 49 | 59 | 52 | 65 | 61 |

| High Street Partners | 1 | 3 | 9 | 56 | |

| Assured Partners | 26 | 38 | 44 | 38 | 51 |

| World Insurance Associates | 5 | 9 | 18 | 42 | 49 |

| Alera Group | 38 | 28 | 24 | 18 | 45 |

| Broadstreet Partners | 32 | 34 | 34 | 58 | 45 |

| Relation Insurance | 2 | 6 | 11 | 33 | |

| Patriot Growth Insurance Services | 25 | 21 | 31 | ||

| The Hilb Group | 14 | 12 | 25 | 22 | 25 |

| Gallagher | 30 | 36 | 34 | 23 | 24 |

| Risk Strategies Company | 11 | 10 | 22 | 18 | 24 |

| One Digital | 13 | 27 | 17 | 32 | 20 |

P&C agencies still the most sold

P&C sellers accounted for 53% of all of agency acquisitions in 2021 or 547 of the total 1,034 transactions.

“The industry is in unprecedented times. We’re coming off a six-quarter stretch that heretofore seemed unthinkable,” said Tim Cunningham, managing partner of OPTIS Partners.

“The brokerage industry continues to prove resilient to economic challenges ranging from terrorism to economic meltdowns and even COVID. Investors love this resiliency and predictability. While private-equity investors will likely be able to absorb increases in loan interest rates, we will be paying attention to their leverage. This has gone under-noticed for a couple of years but may become a hot topic if rates increase significantly.”

How to access the full report

OPTIS Partners’ full report can be accessed here.

{kind=link}