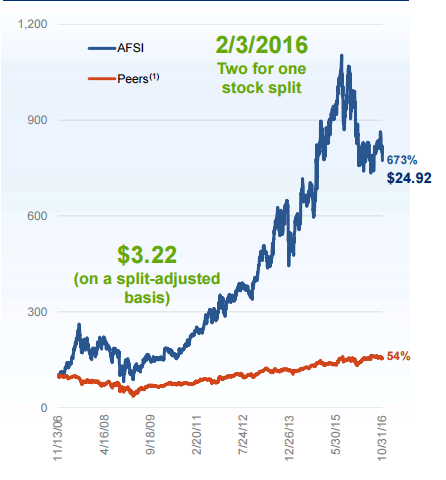

AmTrust Financial Services, Inc. (“AmTrust”), a rapidly growing national insurer, has increased its premium writings over the last ten years at an average rate of 25% per year. In 2016, it reported gross written premiums of $7.9 billion up over 17% from the $6.8 billion of 2015. Likewise, AmTrust public stock price has been a star performer, up over 673% as of November 2016, from the company’s initial public offering in December 2006.

In 2014, AmTrust increased its presence in Massachusetts through acquiring the Tower Group’s commercial lines business. The Tower Group acquisition was only one of 41 acquisitions AmTrust made over the last ten years.

AmTrust’s spectacular growth in especially the last five years has caused some stock analysts and the Wall Street Journal’s sister publication Barron’s to publish articles questioning AmTrust’s reserving and financial accounting. AmTrust has vigorously defended its reserving and accounting practices.

On February 27, 2016 and again on March 17, 2016, though, AmTrust issued press releases that announced a $65 million charge to strengthen reserves, a change of CPA firms, and the imminent restatement of its financial reports for 2014, 2015, and the first three quarter of 2016. As a result, from the first press release to March 20th, AmTrust’s stock lost almost 40% of its value.

With ten years of double-digit growth AmTrust becomes 4th largest comp writer in U.S.

AmTrust writes property and casualty insurance in the United States and internationally. Its three business units comprise small commercial business; specialty risk and extended warranty; and specialty programs. AmTrust distributes its policies through a network of retail and wholesale agents, and through third-party brokers, agents, retailers, or administrators.

AmTrust’s management asserts that much of his success in writing in the U.S. commercial insurance market results from its “differentiated approach to ensuring small businesses.” The company’s target market is “lower-risk, underserved businesses” including restaurants, retailers and professional services. In this market alone, the company’s average premium is $10,000.

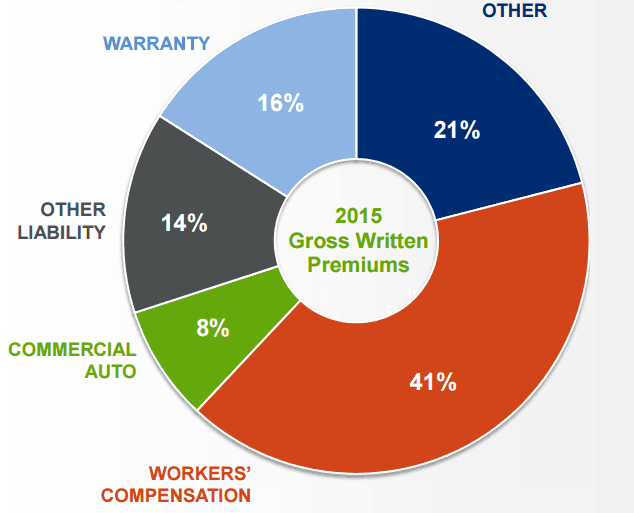

Even within this under-served market that AmTrust has claimed to identify and exploit, AmTrust has further developed what the company identifies as a “Differentiated workers’ comp franchise in [the] small business market.” Workers’ compensation premium made up 74% of AmTrust’s commercial business unit with the other 26% of that unit’s gross written premium resulting from commercial packages and “other low-hazard P&C products.”

Amtrust’s focus on workers’ compensation insurance resulted in the company becoming the 4th largest writer of workers’ compensation in the country by 2015, with $2.7 billion in written premium. See Agency Checklists’ article of April 11, 2016, “The Top Workers Comp. Insurers in the U.S v. Massachusetts.”

The chart to the left demonstrates the company’s focus on workers’ compensation.

The company reaches its target market through over 8000 retail and wholesale agents. The company’s profile of these agents’ premium writings evidences a focus on broad distribution through relatively small books of business per agent. The chart to the right shows the distribution of AmTrust’s agency plants writings.

Management states that the company’s business model essentially capitalizes on highly fragmented markets, that are overlooked by larger competitors, and uses proprietary technology to minimize the business’s loss ratio (net claims paid out). With this business model, the company has generated astounding revenue and earnings growth for many consecutive years.

Management states that the company’s business model essentially capitalizes on highly fragmented markets, that are overlooked by larger competitors, and uses proprietary technology to minimize the business’s loss ratio (net claims paid out). With this business model, the company has generated astounding revenue and earnings growth for many consecutive years.

Average earnings growth of 35% over last five years

Since its initial public stock offering in 2006, the insurer has been dramatically successful in growing its business with returns on equity that appear to be twice that of other carriers. AmTrust’s revenue has grown at an average annualized rate of about 35.3% during the past five years.

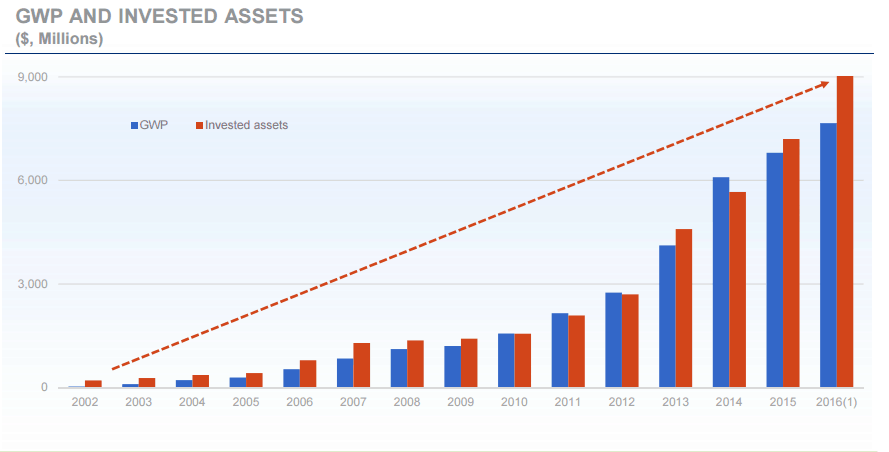

Its gross written premium (“GWP”) and invested assets have also grown at a rate consistent with superior results on the chart below from AmTrust’s November 16, 2016 Investor Day Presentation:

AmTrust’s claim of being a smarter bear leads to questions on reserving and accounting practices

Amtrust’s spectacular financial results and increasing stock price, over the last ten years, have led some stock analysts to question the reserving and financial practices the company. The respected financial newspaper, Barron’s, wrote articles in both 2014 and 2016, questioning whether the company’s financial success resulted from inadequate reserving and financial legerdemain that masked the true state of the company’s affairs.

The articles questioned whether the company was under-reserving on its claims to make the bottom line appear more profitable. Further questions arose around the company’s use of a Luxembourg captive reinsurer, owned by AmTrust, for loss cessions and the approximately $1.4 billion balance sheet item, “other assets.” The “other assets” comprised a loan to a Bermuda reinsurer, ACP Re, controlled by AmTrust’s majority shareholding family, investments in life-settlement contracts, receivables from the company’s extended-warranty business and deferred-tax assets.

The stock market brushed off the concerns voiced over the company’s accounting in 2014. AmTrust’s common stock went from $16.00 a share on a split-adjusted basis to almost $35.00 in 2015. On February 24, 2017, the stock closed at $27.00 before settling into the $27.00 range in February 2017.

Delayed 10-K, restating of financials and $65 million reserve charge drops stock almost 40%

On Friday, February 24, 2017, AmTrust stock closed at $27.66. A little over three weeks later it closed almost 40% lower on Monday March 20, 207 at $16.82. Two press releases, three weeks apart, caused the precipitous drop in AmTrust’ stock price.

On Monday, February 27, 2017, AmTrust issued a press release announcing the company’s fourth-quarter 2016 and full-year 2016 results. The full-year results were impressive.

- Total revenue was $5.45 billion, an increase of $837.7 million, or 18%, from $4.62 billion in 2015.

- Gross written premium was $7.95 billion, an increase of $1,149.7 million, or 17%, from $6.80 billion in 2015.

- The 2016 combined ratio was 92.1%.

- Stockholder’s equity increased 27.0% in the year from $2.75 billion to $3.5 billion.

However, the press release also advised that AmTrust had taken a charge of $65 million, primarily related to strengthening of prior year loss and loss adjustment reserves in its specialty program segment. Worse, the press release also advised investors that AmTrust had “identified material weaknesses in its internal control over financial reporting…”

Notwithstanding the reported results, the reserve charge and the financial reporting “weakness” spooked the stock market and the company’s stock dropped 19% in one day.

AmTrust also had advised in its February 27th press release that it was exercising its right to an automatic extension to file its annual 10-K report with the S.E.C. With the extension, AmTrust’s report would be scheduled for filing on March 16, 2017.

On March 16, 2017, the day by when AmTrust had advised it would file its annual 10-K report, the company issued a second press release advising that the company would not be filing its required as scheduled because of the need for:

- the Company’s outstanding consolidated financial statements for 2014 and 2015 and for the first three quarters of 2016 should no longer be relied upon as they had to be restated.

- the Company’s earnings and press releases for the same periods should no longer be relied upon.

- Additionally, the reports of the Company’s former independent auditor, on the Company’s consolidated financial statements for 2014 and 2015, including its opinions on the effectiveness of internal control over financial reporting for such periods, “likewise should no longer be relied upon.”

The next day, St. Patrick’s Day, March 17, 2017, the company stock dropped another 18%. By Monday, March 20, 2017, the stock had reached $16.82, almost 40% below it price on the trading day before the company’s first press release

A. M. Best maintains A-rating but reduces outlook from stable to negative

On July 8, 2016, A.M. Best affirmed the financial strength rating of AmTrust as A-(Excellent) with a stable outlook.

Once AmTrust’s February 27, 2017 press release became public, however, A. M. Best issued a revision at 9:10 PM that same evening reaffirming AmTrust’s “A” rating, but revising the company’s outlook to “negative.”

The negative rating actions, per A. M. Best, followed the announced delay in filing AmTrust’s annual report and AmTrust’s identifying “material weaknesses related to its internal controls over: the assessment of risks associated with financial reporting; and corporate accounting and corporate financial reporting resources within the company.”

When AmTrust issued its March 17, 2017 press release announcing that the company annual 10-K report to the S.E.C. would not be filed as scheduled but would be filed “as soon as practicable,” A. M. Best elected to “wait and see.” The rating agency issued its own press release maintaining AmTrust’s “A” rating with a negative outlook. However, its announcement stated

The delay in the…[10-K] filing and announced restatement of [ AmTrust’s] previously filed financial statements for 2014 and 2015 place additional negative pressure on its ratings.

* * *

Until the 10-K is filed, A.M. Best cannot determine the extent to which the change in the restated financial results may be material to its assessment of the ratings of AFSI or its subsidiaries. The negative outlook reflects the potential for negative rating action to be taken if the differences in the restated financial results are sufficiently material to cause a reassessment in A.M. Best’s view of the company’s financial condition.”

Class action suits filed as lawyers advertise for investors who lost money on AmTrust stock

On February 28, 2017, the day after the first press release, class actions lawyers flooded the Internet with advertisements for AmTrust’s stockholders looking to sue AmTrust .

As of March 20, 2017, at least six class actions, if not more, had been filed against AmTrust and certain of its officers alleging they made materially false and/or misleading statements and/or failed to disclose that:

(1) AmTrust had ineffective assessment of the risks associated with the financial reporting;

(2) AmTrust had an insufficient complement of corporate accounting and corporate financial reporting resources within the organization;

(3) as a result, AmTrust lacked effective controls over financial reporting; and

(4) consequently, defendants’ statements about AmTrust’s business, operations, and prospects, were materially false and misleading and/or lacked a reasonable basis at all relevant times.

Based on the disclosures made by AmTrust regarding its lack of adequate financial controls, many additional lawsuits will likely be filed. Since security class actions are almost always federal suits, the individual law suits are usually consolidated in one federal district court under the federal rules for complex litigation.

AmTrust developed a Massachusetts presence acquiring Tower Group’s commercial lines

Although by 2014, AmTrust was one top ten writer in the country of workers’ compensation, it gained a larger presence in the Massachusetts market only through the acquisition of the commercial renewal rights of another high-flying, fast-moving insurance holding company, the Tower Group.

Because of under-reserving and inadequate capitalization, the Tower Group essentially had to sell the renewal rights for both the commercial lines and personal lines held by the Tower Group subsidiaries to AmTrust and National General Insurance Group, respectively. See Agency Checklists’ article of September 17, 2014, “Tower National and Massachusetts Homeland Insurance garner financial stability with merger.”

While AmTrust is a much larger company, it is important to note that the Tower Group started its own downward spiral when it began announcing reserve charges and financial reporting issues.