On May 1, 2019, the Workers’ Compensation Rating and Inspection Bureau of Massachusetts (“WCRIB”) began a two-year test program began for voluntary workers’ compensation carriers to use an endorsement that will enable an insurer writing workers’ compensation insurance in Massachusetts to charge an audit noncompliance fee to insureds who do not allow the insurer to audit their policy.

On May 1, 2019, the Workers’ Compensation Rating and Inspection Bureau of Massachusetts (“WCRIB”) began a two-year test program began for voluntary workers’ compensation carriers to use an endorsement that will enable an insurer writing workers’ compensation insurance in Massachusetts to charge an audit noncompliance fee to insureds who do not allow the insurer to audit their policy.

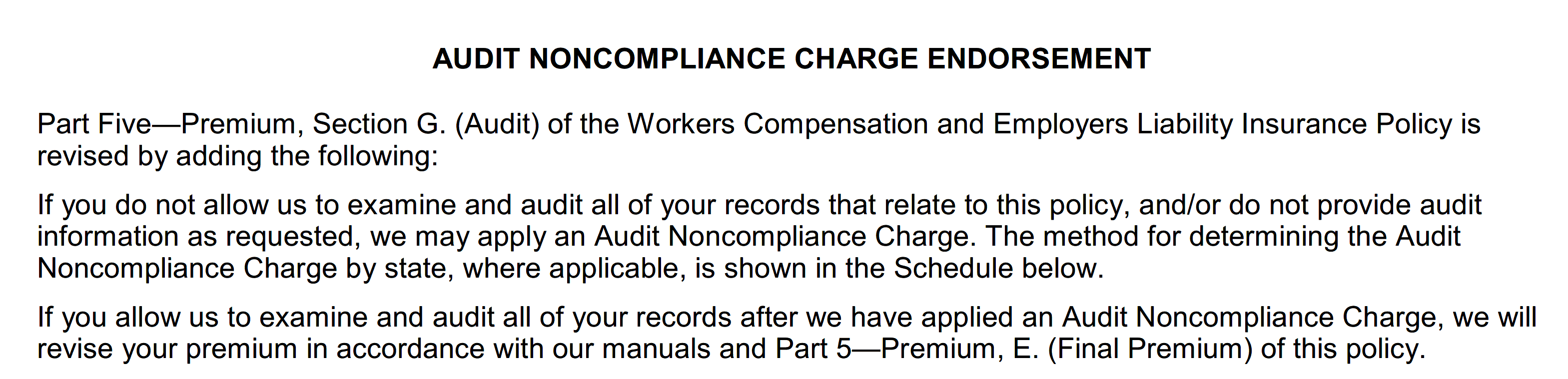

According to the WCRIB filing, the audit noncompliance charge endorsement, developed by the National Council on Compensation Insurers, has been approved in 34 NCCI jurisdictions and by five independent rating bureaus. The new audit noncompliance charge endorsement revises the audit section of the standard workers’ compensation policy to state:

If you do not allow us to examine and audit all of your records that relate to this policy, and/or do not provide audit information as requested, we may apply an audit noncompliance charge. The method for determining the audit noncompliance charge by state, where applicable, is shown in the Schedule below.

If you allow us to examine and audit all of your records after we have applied an audit noncompliance charge, we will revise your premium in accordance with our manuals and Part 5—Premium, E. (Final Premium) of this policy.”

The audit noncompliance charge is twice the policy’s premium

An insured has a contractual obligation to allow an audit of their books and records by their insurance carrier to determine the correct premium due for their remuneration and job classifications. The new endorsement charges an insured who neglects or refuses to all their insurers’ auditors a surcharge equal two times the estimated annual premium measured from the inception of the policy.

An insurer, however, can only charge an audit noncompliance charge if:

- The insured’s policy had an Audit Noncompliance Charge Endorsement attached to the policy at the inception of the term being audited by the insurer;

- The insurer has made two separated attempts to obtain the audit information or complete the audit before applying an audit noncompliance charge;

- The insurer maintains written documentation of its good faith attempts to obtain the audit information and to provide notice of an opportunity to cure, including:

The insured allowing a proper record review purges an audit noncompliance charge

The audit noncompliance charge, as approved by the division for the two-year test, is a compliance incentive. Where the insured initially refuses but eventually permits the audit, an audit noncompliance charge will not be charged.

If an insured refusing an audit pays an audit noncompliance charge but subsequently allows an examination and audit of all records that relate to the policy involved, the insurer will have to refund the audit noncompliance charge to the insured or apply the audit noncompliance charge refund to any additional premium charge resulting from the audit, as the case may be.

Failure to pay an audit noncompliance charge is not ‘nonpayment of premium’ for cancellation purposes

By statute, in Massachusetts, mid-term cancellations of workers’ compensation policies are only allowed for three specific reasons:

- nonpayment of premium;

- fraud or material misrepresentation affecting the policy or insured;

- a substantial increase in the hazard insured against.

These grounds only apply to cancellations and not to an insurer’s right to refuse to renew a workers’ compensation policy.

Based on the Division’s decision on the Stipulation, failure to pay the audit noncompliance charge may not, on its own, give an insurer grounds to initiate mid-term cancellation of the policy for “nonpayment of premium.”

The application of an audit noncompliance charge to the policy does not affect an insurer’s right to cancel mid-term for any of the above three statutory grounds.

New filing required 2021 following a two-year test period

After an earlier withdrawn filing, the WCRIB withdrew, the WCRIB submitted a filing on January 29, 2018, proposing to revise the Massachusetts workers’ compensation manual to allow a policy endorsement and permitting insurers to charge an audit noncompliance fee to insureds who do not allow the insurer to audit their books as required by their workers’ compensation policies.

In approving a revised stipulation allowing for a two-year test period, the two hearing officers assigned to the matter, Jean F. Farrington and Kristina A. Gasson, opined that the new endorsement would have “the salutary goal of collecting data specific to Massachusetts on the use of an audit noncompliance charge as a tool for effective calculation and collection of workers’ compensation insurance premiums.”

The hearing officers did require as part of the stipulation that an insurer using the endorsement could not pick and choose among insureds. The insurer must apply the endorsement to all insureds in a particular business classification or none.

Also, the hearing officers believed that the forms required for explaining and attempting compliance with an audit should remove potential complaints of bias in the selection of audit noncompliance charge recipients or any compliance proceedings.

The hearing officers also noted that the parties to the stipulation, the WCRIB, and the Attorney General recognized that the revised stipulation, approved by the hearing officers and Commissioner Anderson, would only be in effect solely for the two years, beginning May 1, 2019, and ending April 30, 2021. The hearing officers advised that a new filing will be required in 2021, to determine if the audit noncompliance charge endorsement would continue as is, be modified, or while unlikely, disapproved.