There was a 31% increase in insurance mergers & acquisitions activity in 2017

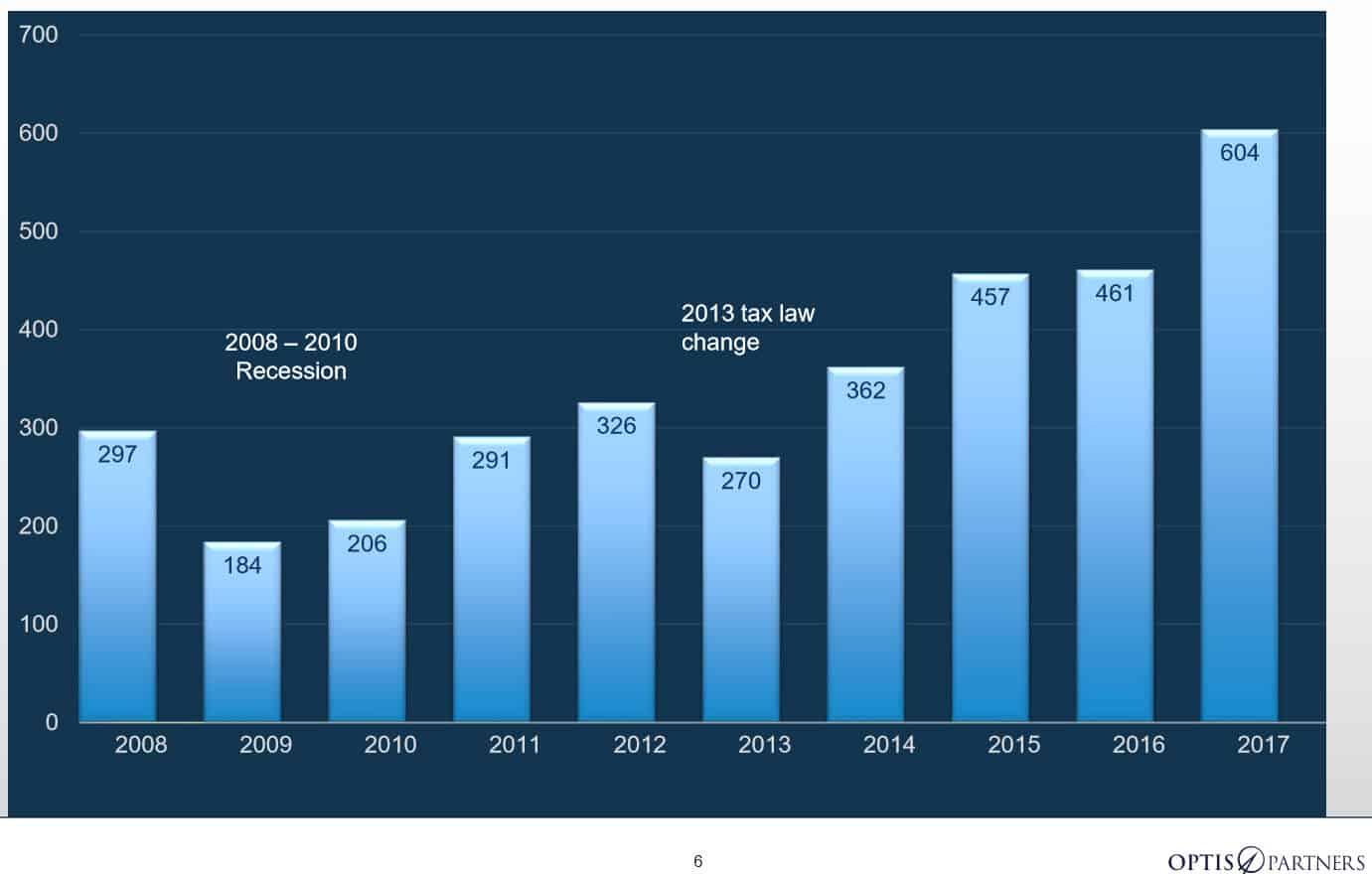

The numbers are in and it’s official, the year 2017 has been far and away the most active year for Mergers & Acquisition with respect to insurance agencies. According to the OPTIS Partner’s annual report recapping 2017, there were 604 announced deals this year. This represents a 31% increase over the 461 deals announced in 2016.

“This whopping increase exceeded expectations,” said Timothy J. Cunningham, managing director of OPTIS, an investment banking and financial consulting firm specializing in the insurance industry, adding that “We expect the beat to go on in 2018.”

The actual number of sales was probably much higher than the 604 reported, noted Cunningham, as many buyers and sellers across the country do not report transactions, along with many acquirers who do not report small transactions.

“The OPTIS database, however, tracks a consistent pool of the most active acquirers, including other announced deals, and is, therefore, a reasonably accurate indication of deal activity in the sector,” he added. The following is a look at the rate of mergers and acquisitions with respect to insurance agencies over the past nine years.

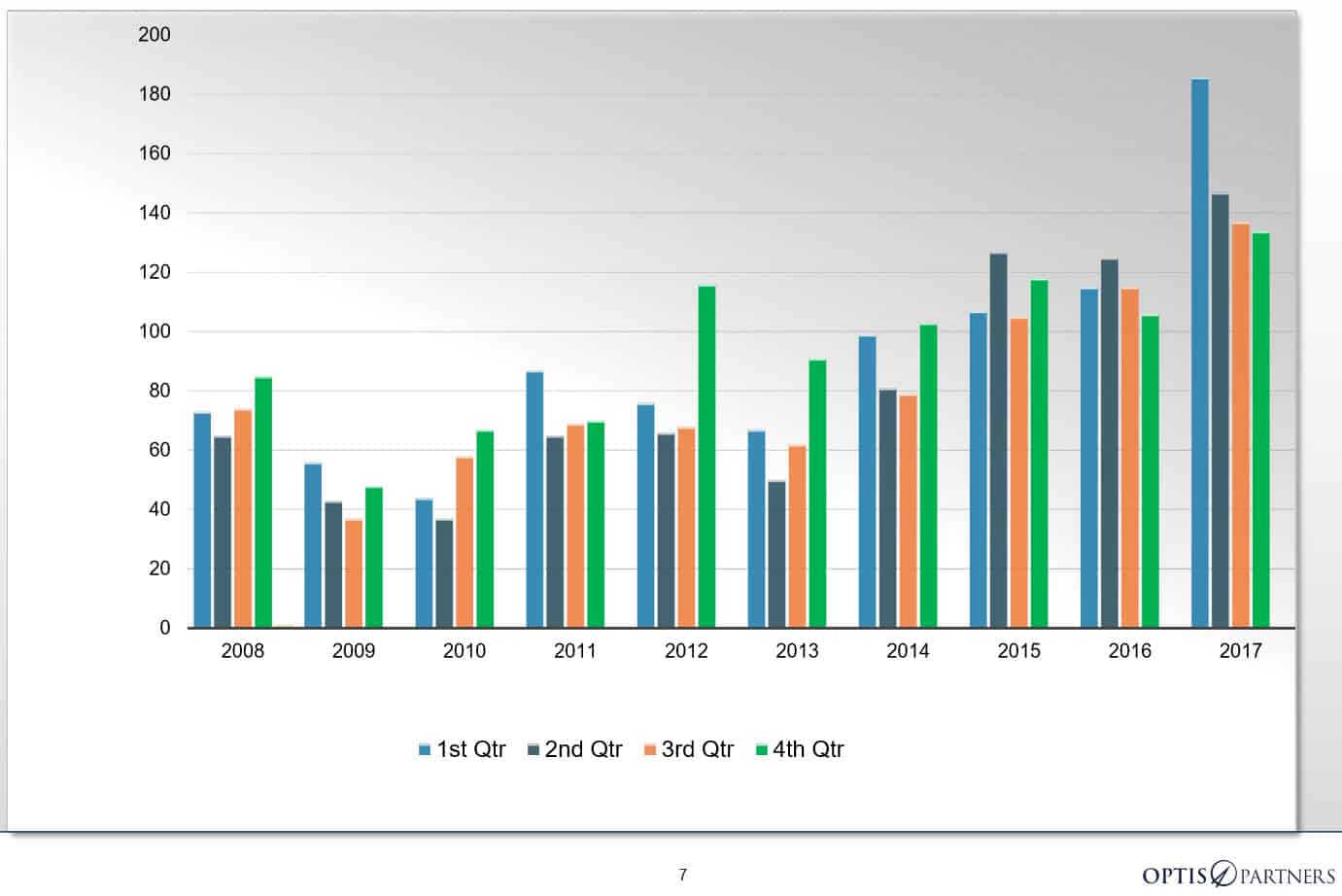

The next chart outlines the rate of insurance agency acquisitions by Year and by Quarter over the same nine-year time period.

Like the company’s quarterly report, OPTIS Partners yearly recap includes data covering U.S. and Canadian insurance agencies that either sell property & casualty insurance, employee benefits, or both P&C and employee benefits. The report also includes transactions involving wholesalers and managing general agency brokerage businesses.

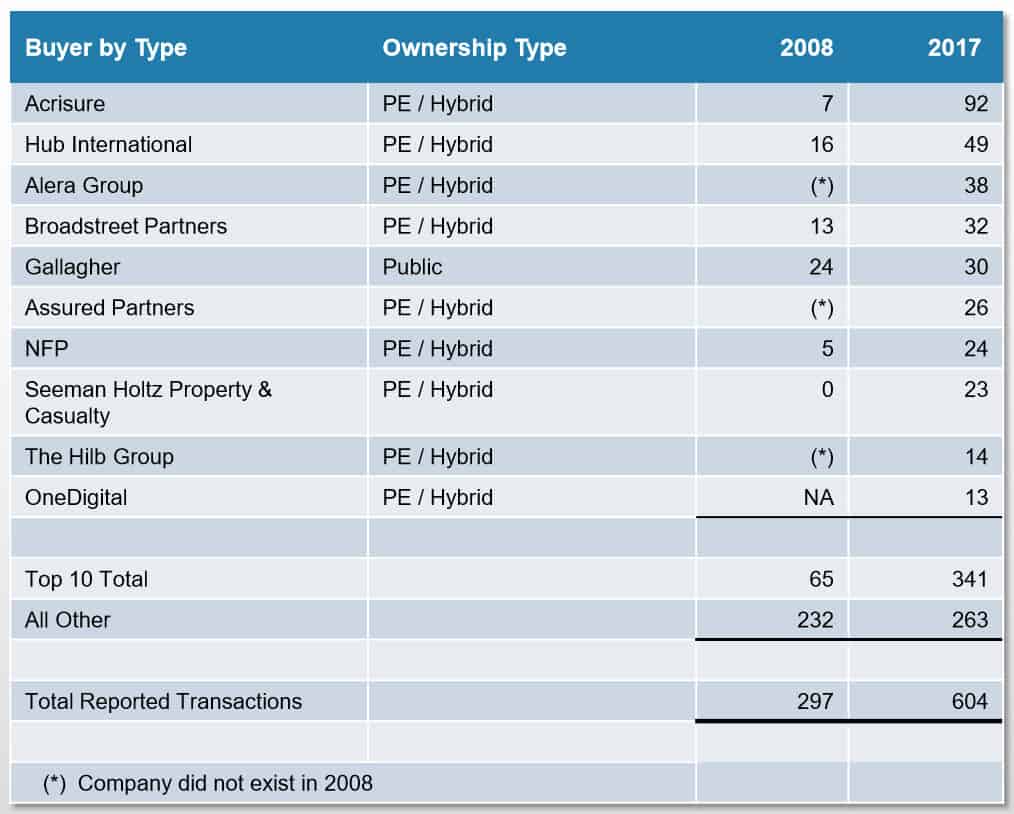

2017 Agency Acquisitions by Buyer Type

For this year’s annual report, OPTIS Partners created a new classification of Buyers, known as PE/Hybrid. This new classification represents the combining of PE or private equity-backed firms, due to the “blurred lines” between these two types of firms. In both instances, both firms receive a “significant amount” of M&A financial support.

Based on this tweaking of the Buyer Groups, there are now five Buyer categories in which the 2017 transactions have been grouped:

- Publicly Traded ,

- Privately owned ,

- Private-Equity owned and very active privately owned, all with acquisition capital support from their PE Sponsor, outside lenders and/or internal cash flow, will be referred to as “PE / Hybrid” buyers,

- Banks and financial institutions,

- Other (Insurance companies, non-insurance industry)

With these new classifications, the newly created PE/Hybrid Group was involved in the greatest number of mergers & acquisitions, completing 382 of the 604 reported transactions last year. This represents approximately 63% of all mergers & acquisitions. This number is a 56% increase over this buyer group’s activity in 2016.

So who were the top agency buyers this past year?

Unsurprisingly, the majority of the most active acquirers this past year belong o the PE/Hybrid classification as depicted in the following list of the top ten buyers.

And who were the top sellers?

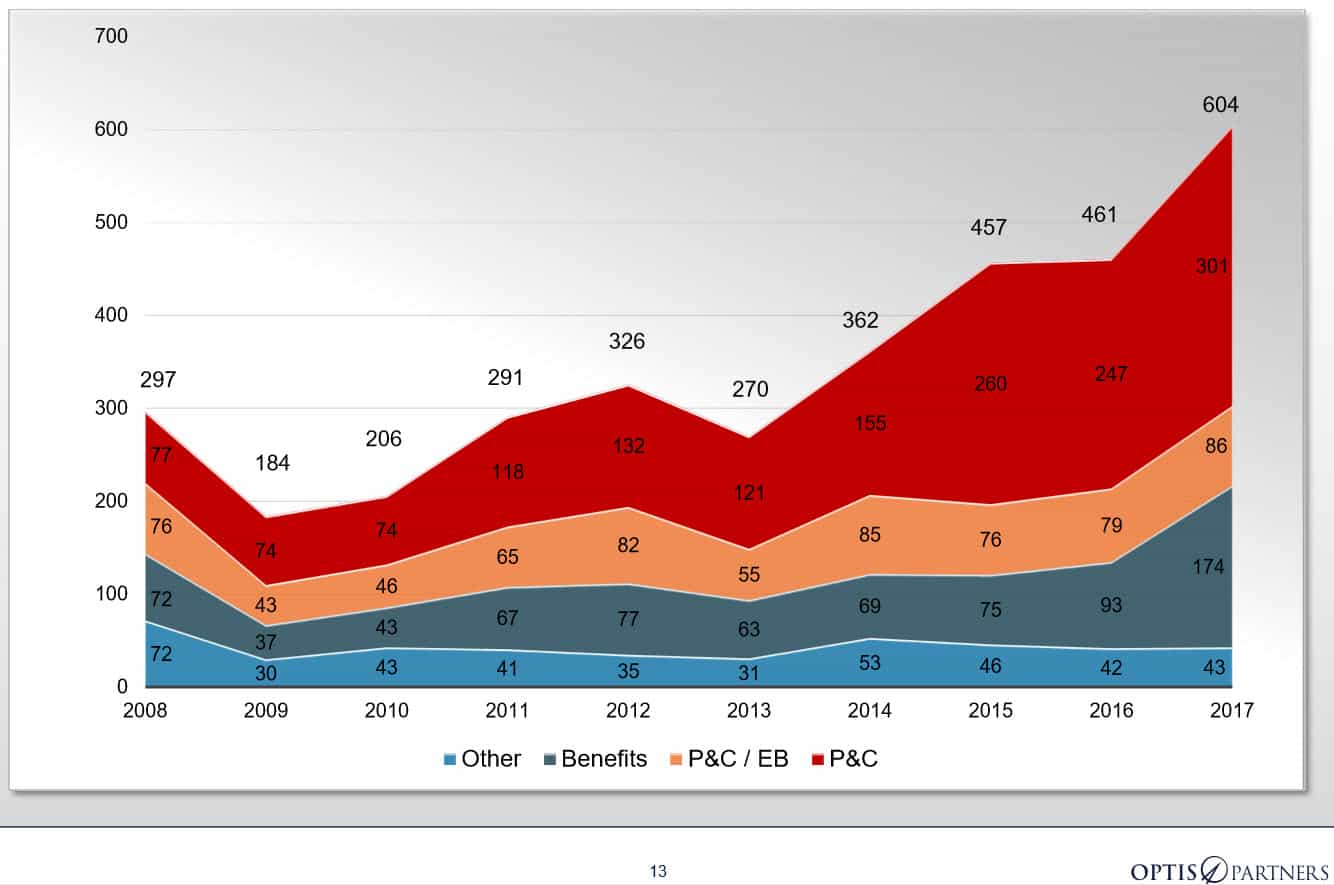

According to the company’s research, Property & Casualty sellers remained the main target of acquisition, with 301 announced transactions. The sale of Employee Benefits firms, however, witnessed a dramatic increase in acquisitions, almost doubling in number from 93 deals noted in 2016 to 174 in 2017.

Interestingly, the report also notes that 86 deals last year involved insurance agencies selling both Property & Casualty as well as Employee Benefits coverages. In addition, there were additional 43 sales involving the “other” category which is made up of managing general agents, third-party administrators and other types of sellers.

As a result of these statistics, OPTIS Partner Daniel P. Menzer has identified the following key lessons:

- The inventory of interested sellers remains high.

- It’s hard to perpetuate agencies internally. Third parties are willing to pay much more than internal buyers. Few agency owners will leave that much money on the table.

- A strong economy, a stable insurance market, and easy access to relatively inexpensive capital for buyers all spurred activity.

- There are plenty of investors and lenders willing to fund PE/hybrid buyers.

- If you’re a buyer, pay attention to cash flow and be careful not to overpay.

- If you’re a seller, identify the best cultural and operational fit. Take advantage of strong pricing before things change.

Observations on the Massachusetts marketplace

Turning towards Massachusetts, according to OPTIS Partners and Agency Checklists’ records, there were a total of 25 announced (plus two unannounced) mergers and acquisitions in the Commonwealth during 2017. This number was done from the 32 transactions reported in 2016, but was still enough to make Massachusetts a top seller state. In fact, OPTIS Partners data reveals Massachusetts as one of the top ten seller states last year.

Unlike the rest of the country, however, the largest buyers of P&C agencies in the Commonwealth continue to be local, privately-held insurance agencies.

So even though, M&A activity has been strong here in the Commonwealth, the majority of the buyers and sellers continue to be connected to the Massachusetts insurance industry rather than from outside of it.

What is happening right here in Massachusetts?

The following are the agency acquisitions that Agency Checklists has tracked and written about so far in 2017.

January 2017 (Q1)

Risk Strategies Acquires Quincy’s University Health Plans

February 2017 (Q1)

Eastern Insurance Acquires the Historic Chase & Lunt Insurance Agency, LLC

Rhode Island’s Starkweather & Shepley Acquires Its Second Mass. Agency In Sturbridge

March 2017 (Q1)

The Hilb Group Acquires The Groups Benefits Division of Mass.-based Sapers & Wallack, Inc.

Wheeler & Taylor Insurance Acquires Great Barrington Office of Goodworks Insurance

April 2017 (Q2)

Mass. Agencies The HR Hatch Insurance Agency and Nancy Z. Bender Insurance Announce Merger

McGowan Purchases Assets of North American Professional Liability Insurance Agency, LLC (“NAPLIA”)

Risk Strategies Acquires Lynnfield’s Mosse & Mosse Associates

May 2017 (Q2)

Workers Credit Union Acquires Worcester’s Braley & Wellington Group

WTPhelan Acquires The Cronin Insurance Agency

Cross Insurance Acquires Weymouth’s A.E. Barnes Insurance Agency

Liberty Mutual Acquires TRU Services

June 2017 (Q2)

Kiley & O’Toole Announces Acquisition Of Baltic Insurance

Cross Insurance Acquires Massachusetts’ Appleby & Wyman Agency

July 2017 (Q3)

The McGowan companies purchases Assets of Framingham’s NAPLIA

Liberty Mutual Insurance Acquires Assets of Medical Stop Loss Provider TRU Services, LLC

August 2017 (Q3)

One unannounced transaction

September 2017 (Q3)

Massachusetts’s “Five Star” Agency, Mid-State Insurance, Purchased by The Hilb Group

October 2017 (Q4)

One unannounced transaction

November 2017 (Q4)

Burgin Platner Hurley Insurance Acquires the Brendon Potter Insurance Agency

Massachusetts’ HR Knowledge Acquired By The Hilb Group

December 2017 (Q4)

Hub International Acquires Summit Financial Insurance Agency

Our exclusive list of M&A transactions in Massachusetts

Please note that while we try and keep our own data up-to-date as much as possible, we cannot guarantee that we have included every transaction that has taken place in the Commonwealth so far this year.

If you know of an agency that was bought or sold and does not appear on this list, please help us out by letting us know here.