Massachusetts Leads Nation in EV Insurance Premium Gap

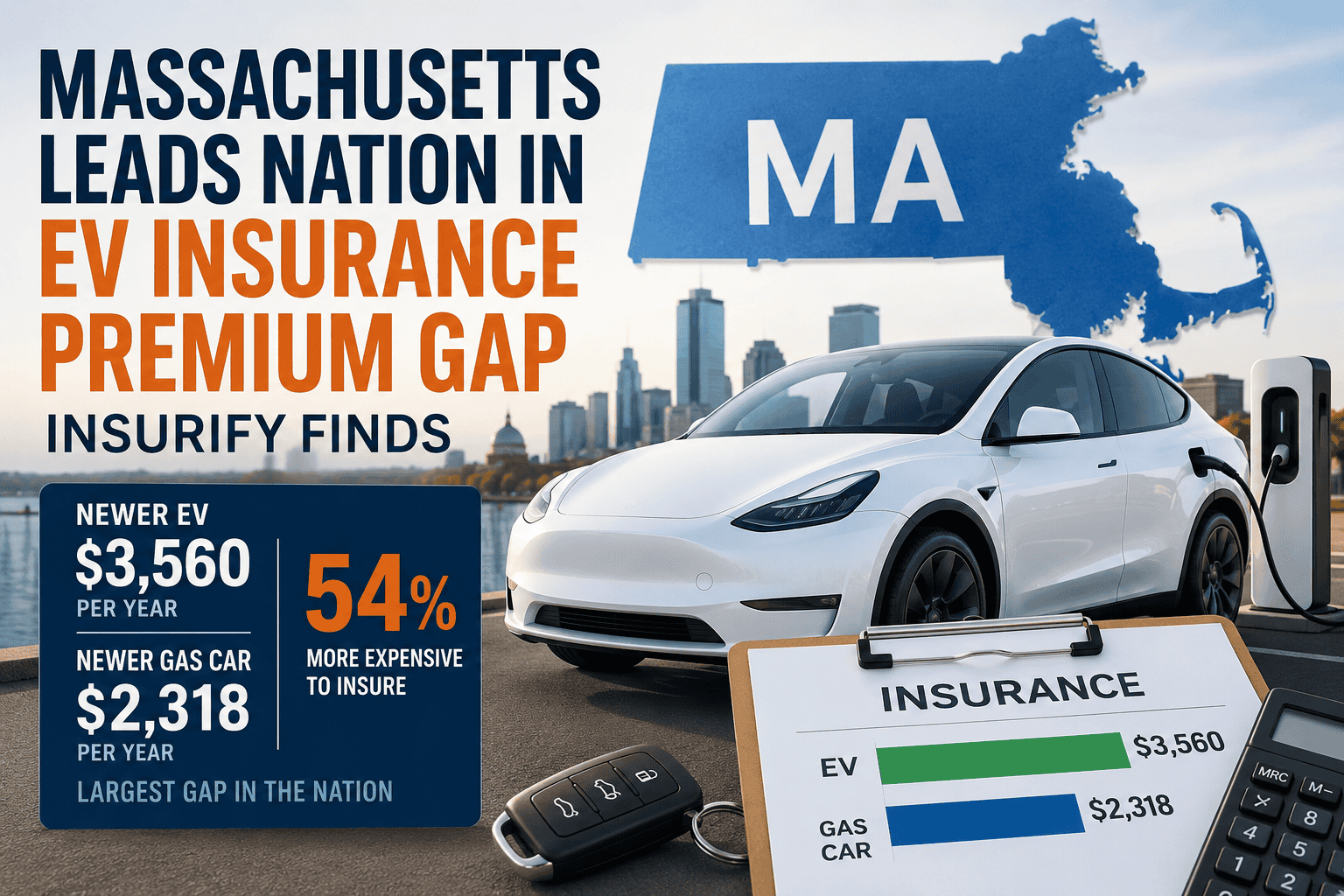

Massachusetts drivers pay the highest electric vehicle insurance premium surcharge in the nation, according to a new Insurify analysis of more than 235 million insurance quotes. The study found that insuring a newer electric vehicle in Massachusetts costs 54% more than insuring a comparable gas-powered vehicle, the largest gap among all states.

For insurance professionals, the findings highlight how vehicle technology, repair costs, and local market conditions continue to influence claim severity and pricing, even as overall auto insurance rates have begun to moderate.

Massachusetts Stands Apart From National Trends

Nationally, electric vehicles remain more expensive to insure than gas-powered vehicles, but the gap is considerably smaller than in Massachusetts.

Insurify reported that EVs cost an average of $3,159 annually to insure nationwide compared with $2,218 for gas-powered vehicles, a difference of 42%. When comparing only newer vehicles—model year 2024 and newer—the gap narrows to 18%.

Massachusetts, however, showed a much wider disparity. According to the analysis, a newer EV costs an average of $3,560 annually to insure in the Commonwealth compared with $2,318 for a comparable gas-powered vehicle, creating a $1,242 annual difference.

The finding is particularly notable because newer EV insurance costs have been declining nationally. Insurify reported that insurance rates for newer EVs fell 11.1% over the past year, compared with a 7.7% decline for newer gas-powered vehicles.

Repair Costs Continue to Drive EV Premiums

Insurify attributes much of the higher insurance cost for EVs to repair severity.

Electric vehicles contain sophisticated electronics, sensors, battery systems, and advanced driver assistance technology that can increase repair complexity and cost. The report notes that many newer vehicles, regardless of propulsion type, now contain similar technologies, helping narrow the insurance-cost gap between newer EVs and newer gas-powered vehicles.

The report also points to battery-related repair and replacement expenses as a significant contributor to claim severity. In addition, some manufacturers require specialized procedures, including battery removal before certain collision repairs can be performed, increasing labor requirements and repair costs.

Massachusetts Labor-Rate Debate Provides Additional Context

The Massachusetts repair market has been the subject of ongoing debate between insurers and collision repair facilities over labor rates and repair capacity.

Rather than relying on individual industry submissions, the Commonwealth’s Auto Body Labor Rate Advisory Board collected survey data from both insurers and repair shops during 2025. The board received usable responses from 476 registered repair facilities and 16 insurers representing approximately 95% of the Massachusetts private-passenger auto market.

The Advisory Board found that insurers reported paying a weighted-average body labor rate of $49 per hour statewide, with rates ranging from $43 to $55 per hour. Massachusetts repair shops responding to the survey reported an average customer-pay body labor rate of $68 per hour and a median rate of $65 per hour.

For mechanical repairs, insurers reported paying a weighted-average rate of $55 per hour, while repair shops reported average customer-pay mechanical labor rates exceeding $100 per hour.

The Advisory Board did not reach consensus on a recommended statewide labor rate but documented the continuing disagreement between insurers and repair facilities regarding prevailing rates and repair economics.

Multiple Factors May Be Contributing

Insurify’s analysis suggests that Massachusetts’ unusually large EV insurance gap likely reflects a combination of factors rather than any single cause.

The report points to the concentration of higher-value EVs in the Boston metropolitan area, the costs associated with specialized EV repairs, and state-specific market characteristics. It also notes that Massachusetts does not permit insurers to use credit-based insurance scoring, eliminating a rating variable that insurers use in many other states.

Readers interested in reviewing Insurify’s complete June 2, 2026 analysis can access the report, “The EV Premium Penalty: Insuring an EV Is 42% More Expensive Than a Gas Car, but Newer Models Are Closing the Cost Gap,” on Insurify’s website.

Taken together, those factors appear to be producing a Massachusetts market where EV claim costs remain sufficiently elevated to create the largest premium differential in the country, despite a broader national trend toward narrowing insurance-cost gaps between electric and gas-powered vehicles.