The second in a four-part series on the Annual Home Insurance Report

This is the second part of a four-part look at the Commissioner’s Annual Report on Home Insurance in Massachusetts. Since 1996, the DOI has been required to produce a home insurance report pursuant to M.G.L. c. 175 Sec. 4A & 4B. Unlike private passenger auto insurance in Massachusetts, however, there are no laws requiring that a property owner have home insurance. Please note all of the charts and graphs come courtesy of the Annual Home Insurance Report.

As mentioned in our First Look article last week, this year’s report cites a 3.12% increase, or 60,176 policies, in the overall number of home insurance policies in the Commonwealth between 2016 and 2017. This is a marked increase from the year before when the Division noted that there was only a .04% increase in policies from 2015 to 2016.

This week, we review the Commissioner’s findings concerning Home Insurance within the MA FAIR Plan. Following the trend of the past few years, total enrollment in the MA FAIR Plan continues to lose market share. While the MA FAIR Plan continues to write a majority of the home insurance in the Commonwealth, particularly on the Cape and Islands, it has substantially decreased its number from the levels seen in 2007.

What is the FAIR Plan and what does it do in Massachusetts?

What is the FAIR Plan and what does it do in Massachusetts?

For those homes which cannot obtain coverage from a traditional homeowner’s insurance company, the home’s owner may apply to the Massachusetts Property and Underwriting Association, commonly referred to as the FAIR Plan, which is required by statute to obtain a homeowner’s policy with a replacement cost of up to $1 million dollars. For those homes, traditionally waterfront properties, that may have a value of more than 1 million dollars, a homeowner must seek coverage via the surplus lines market.

FAIR Plan continues to write the largest amount of homeowner’s insurance on Cape Cod

In general, the proportion of FAIR Plan policies in force varies significantly by geographic area. Even though the total enrollment in the FAIR Plan decreased by 2,332 policies in 2017, it now only rights approximately 10.7% of the total amount of home insurance premium in the Commonwealth. The largest majority of FAIR Plan policies is concentrated on the Cape and Islands (which comprises Barnstable, Dukes, and Nantucket counties). While this area still has a large share of FAIR Plan policies, the FAIR Plan’s share here also has continued to decrease with it now writing approximately 40% of all homeowners policies here. This represents a 3.3% decrease in Market Share since the last time Agency Checklists reviewed these numbers.

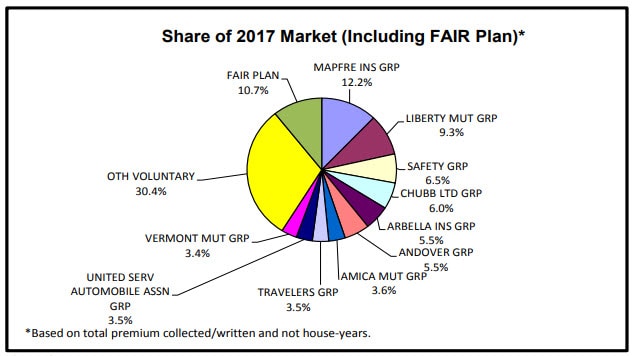

MAPFRE continues as the largest homeowners insurer in Massachusetts with a 12.2% percent market share. The FAIR Plan is now only just in front of Liberty Mutual with a 10.7% market share to Liberty Mutual’s 9.3% share. Rounding out the larger remaining market shares are Safety, Chubb, Arbella, Andover, Amica, Travelers, USAA, and Vermont Mutual.

As the Division noted in its report, unlike many other states, the majority of homeowners’ insurance companies continue to be locally-based insurers.

The rise and fall of FAIR Plan policies over the past decade

As this ten-year retrospective demonstrates, the total amount of FAIR business has been steadily decreasing during the past decade. According to the DOI, the FAIR Plan’s peak was in 20017 when it claimed a 16.1% market share. Since then, when it had a total of 204,101 policies, the FAIR Plan as of 2017 now has a total of 183,745 policies.

Once in, few leave the FAIR Plan

The failure of consumers to leave the FAIR Plan once they have been assigned to it is one of the major problems cited in the annual Home Insurance Report. Only 11 policyholders of the almost 199,500 policies written through the FAIR Plan, during 2017, took advantage of its Market Assistance Plan, which offers applicants coverage to all other insurers writing homeowner’s insurance within the marketplace.

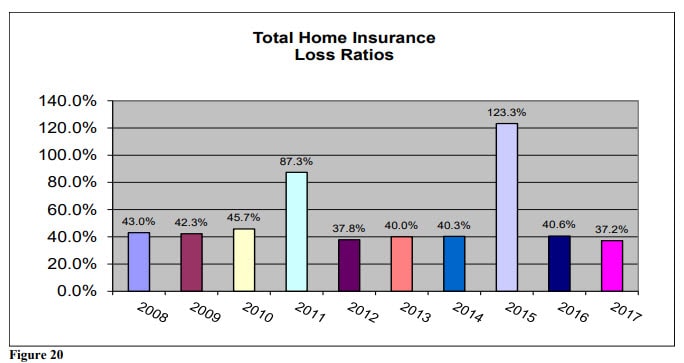

The lowest home insurance loss ratios in Massachusetts over the past ten years

The graph below represents the various loss ratios in Massachusetts over the past ten years. In insurance metrics, loss ratio is an industry-accepted method of measuring the underwriting success or failure of a property insurer. To obtain a loss ratio, losses incurred must be divided by earned premium. As the Division notes,

The higher the cost to the company of reinsurance and other expenses, the lower the company’s loss ratio must be for it to continue to operate. The higher the loss ratio, the more likely companies will have overall losses after paying for administrative expenses.

With that said, we turn to the overall loss ratios for homeowner insurance companies in Massachusetts, including the FAIR Plan. The year 2017 saw another decrease in the loss ratio to 37.2%. This number reflects all types of insured residences (homes, condos, and rentals. This represents the lowest loss ratio over the past decade. The lack of a major weather event was one of the main reasons cited by the DOI for the low loss ratio in 2017.

With respect to which types of homeowners policies had the highest number of losses, condo policies were first with 41.7%, followed by traditional homeowners policies with 37.4%. Tenant policies had the lowest loss ratio by form with 21.4%.

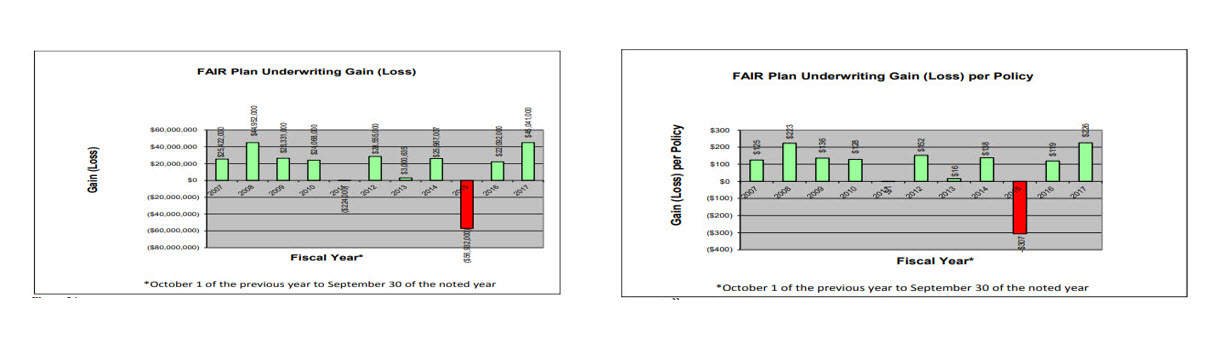

2017 FAIR Plan Financial Results

In 2017, the MA FAIR Plan had a total underwriting profit of $45,041,000 based upon its calendar year of October 1st until September 30th. The number is qualified as the FAIR Plan’s “contribution to surplus” since the FAIR Plan cannot be technically categorized as an insurance company. As illustrated in the Chart, the only loss the FAIR Plan has suffered in the past decade was in 2015. The Division notes that the FAIR plan has not experienced an underwriting loss for the past three years. The last one to occur was in 2011.

When calculated per policy, this means that in 2017, the underwriting gain per policy was $245, approximately $126 more than in 2016. Over ten years, however, the $245 is on the higher end of the scale, and more in line with the FAIR Plan’s contribution to surplus per policy in 2008. As for loss per policy, 2015 was the year in which the FAIR Plan experienced an underwriting loss of -$307 per policy. The Division calculates the FAIR Plan’s Gain (Loss) per policy by dividing the fiscal year’s underwriting profit (or loss) by the number of fiscal year owner, condo or tenant policies issued.

When calculated per policy, this means that in 2017, the underwriting gain per policy was $245, approximately $126 more than in 2016. Over ten years, however, the $245 is on the higher end of the scale, and more in line with the FAIR Plan’s contribution to surplus per policy in 2008. As for loss per policy, 2015 was the year in which the FAIR Plan experienced an underwriting loss of -$307 per policy. The Division calculates the FAIR Plan’s Gain (Loss) per policy by dividing the fiscal year’s underwriting profit (or loss) by the number of fiscal year owner, condo or tenant policies issued.

FAIR Plan Home Insurance Rates Retrospective

The year 2013 was the last year in which the FAIR Plan submitted an overall statewide rate increase of 6.8%. In 2014, the Commissioner denied the rate increase, stating that the FAIR Plan had failed to meet its burden of support in demonstrating that its rate increase satisfied the statutory requirements. The last time that a rate increase was approved was in 2005 when the FAIR Plan was granted a 12.42% statewide increase in rates, along with a 25.0% increase in Barnstable, Dukes, and Nantucket.

The following chart is a ten-year retrospective the Division created representing FAIR Plan Home Insurance Rate Changes.

More to come on the Annual Home Insurance Report in the coming weeks

Next week, Agency Checklists will review take a look at the number of home insurance policies by county followed by further articles on the impact of auto insurance and flood insurance on this market as well as financial results from the report.