Independent agency channel maintains a strong position amid improving underwriting results

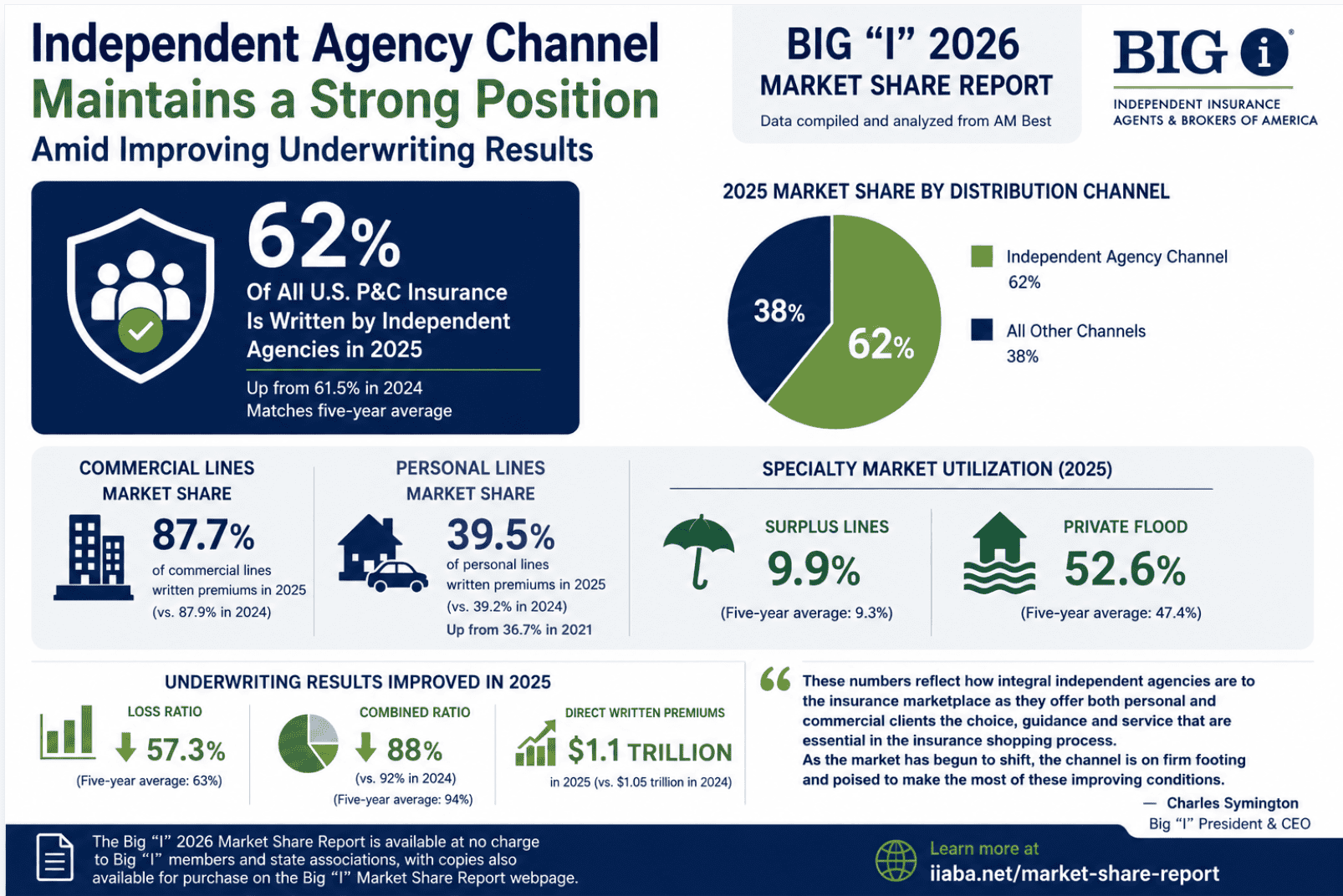

The independent agency distribution channel continues to maintain a healthy position in the U.S. property and casualty insurance market in 2025. According to the latest data from the Big “I” 2026 Market Share Report, approximately 62% of all P&C insurance is written by the independent insurance agency system.

The annual report, which compiles and analyzes property and casualty premium data from AM Best, provides deep insights to agencies and carriers alike to measure market share by distribution channel.

Here are the main takeaways:

Independent agencies maintained—and slightly increased—their market dominance

Based on 2025 data, the report found the independent agency channel increased its overall market share slightly from 61.5% in 2024 to 62% in 2025, matching its five-year average despite what the report describes as the challenges of the hard market.

Independent agencies continued gaining share in personal and specialty markets

Independent agencies also continued to dominate the commercial lines market, writing 87.7% of commercial lines written premiums in 2025, slightly less than the 87.9% written in 2024.

As for personal lines, the channel’s market share continued its gradual upward trend, increasing to 39.5% in 2025 from 39.2% in 2024. Overall, personal lines market share has grown 2.8% since 2021, when it was 36.7%.

The report also found increased utilization of independent agencies in several specialty markets. Surplus lines utilization reached 9.9%, compared with the five-year average of 9.3%, while private flood utilization increased to 52.6% from the five-year average of 47.4%.

“The resilience of the independent agency channel is evident in this year’s Market Share Report, painting a clear picture of its stability through the hard market,” says Charles Symington, Big “I” president & CEO.

Underwriting performance improved significantly

There was a marked improvement in underwriting results during 2025.

Loss ratios declined to 57.3%, compared with the five-year average of 63%. Combined ratios also improved, falling to 88% from 92% in 2024 and below the five-year average of 94%.

At the same time, direct written premiums increased to $1.1 trillion in 2025, up from $1.05 trillion in 2024.

Big “I” Cites Channel Stability

In commenting on the gains made by the independent agency system this year, Symington added:

“These numbers reflect how integral independent agencies are to the insurance marketplace as they offer both personal and commercial clients the choice, guidance and service that are essential in the insurance shopping process. As the market has begun to shift, the channel is on firm footing and poised to make the most of these improving conditions.”

The Big “I”’s 2026 Market Share Report is available at no charge to Big “I” members and state associations, with copies also available for purchase on the Big “I” Market Share Report webpage.