Deals for P&C and benefits brokers in United States and Canada slip as market consolidation continues

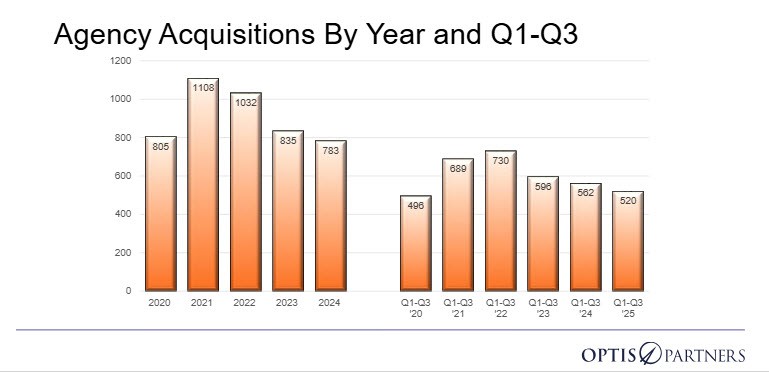

The pace of insurance agency mergers and acquisitions across the United States and Canada slowed slightly in 2025, with total announced deals through the third quarter down 7% year over year, according to OPTIS Partners’ latest M&A report.

Overall, 520 transactions have been counted during the first three quarters of 2025, as compared to 560 during the same period in 2024. Deal volume, however, accelerated during the third quarter with 188 transactions reported, representing a 5% increase from the second quarter.

“Looking ahead to the fourth quarter, we expect activity to be equal to or slightly below Q4-2024, thus continuing the trend of the last three years,” said Steve Germundson, partner at OPTIS Partners, an investment banking and financial consulting firm specializing in the insurance industry.

BroadStreet Leads as Top Buyer

Among acquirers, BroadStreet Partners remains the most active buyer year to date, announcing 57 transactions compared to 72 over the same period last year. Hub International followed with 38 announced deals.

A number of other buyers increased their activity over the past 12 months, including Alera Group, which reported a 100% increase in deals, HighStreet Partners, which increased by 75%, and King Risk Partners by 53%.

Private Equity Continues to Dominate the Buyer Landscape

OPTIS tracks four buyer categories: private equity-backed/hybrid buyers, privately held brokers, publicly held brokers, and all others.

Private equity-backed/hybrid buyers continued to dominate the market, accounting for 72% of all transactions year to date. This group includes brokerage platforms like BroadStreet as well as institutional investors such as family offices, pension funds, and sovereign wealth funds.

Privately held brokers accounted for 145 deals so far in 2025, while publicly held brokers announced 54 transactions.

“There are interesting dynamics underway. A few new investors are in the market for the first time,” said Timothy J. Cunningham, managing partner at OPTIS Partners. “However, there are fewer active buyers among both private-equity and privately owned categories.”

P&C Agencies Remain the Primary Sellers

P&C agencies remained the dominant seller group, accounting for 336 transactions, or 65% of total deals. The following is a breakdown of the percentages:

- P&C agencies: 336 deals (65%)

- Employee benefits agencies: 75 deals (14%)

- P&C/benefits agencies: 46 deals (9%)

- Other sellers: 63 deals (12%)

Market Context: Fewer Buyers, Consistent Seller Mix

While total deal volume declined year over year, the buyer landscape remains concentrated among private equity-backed platforms and their affiliates. BroadStreet Partners continued its role as the largest acquirer in the marketplace. The increase in activity from Alera Group, HighStreet Partners, and King Risk Partners points to ongoing competitive dynamics among active consolidators.

On the sell side, the composition of transactions has changed little. Property-and-casualty agencies continue to make up the bulk of deals, consistent with prior reporting periods.

Outlook for the Remainder of 2025

Germundson noted that current momentum suggests Q4-2025 will likely be on par with or slightly below last year’s fourth quarter, extending a multi-year pattern of steady activity.

The full OPTIS Partners Q3 2025 M&A Report is available at: https://optisins.com/wp/2025/10/q3-2025-ma-report/.