The issue is rarely whether the insured knew the policy was surplus lines. It is whether the file shows why surplus lines was needed.

A loss that arrives three years after binding

A retail agency places a three-family habitational risk in surplus lines after two of its appointed admitted carriers decline. The wholesaler returns a quote with a vacancy condition, a 90% coinsurance clause, and a water-damage sublimit. The producer signs the original-broker portion of Form BR-7. The insured signs and acknowledges that the policy is non-admitted and that the Massachusetts Insurers Insolvency Fund will not respond if the carrier becomes insolvent. The file is closed.

Three years later, there is a fire loss following a brief vacancy. The vacancy clause is invoked. The insured retains counsel. A plaintiff’s expert reviews the file and identifies two admitted carriers — accessible through a regional wholesaler the agency does not regularly use — that were writing similar three-deckers at the time of binding without a vacancy condition or with a much narrower one. MPIUA, on the property side, would also have written the dwelling without that exclusion.

The claim that follows is not “I didn’t know this was surplus lines.” It is:

“My broker should not have placed me there. An admitted market was available, and the broker either did not know about it, did not access it, or did not tell me that another broker might have been able to access it.”

That is the Massachusetts producer’s E&O problem.

The real claim is the diligent-effort claim

Massachusetts producers turn to surplus lines for the right reasons every day — coastal exposures, older or wood-frame buildings, habitational accounts, unusual classes, and liability risks outside admitted appetite. The trouble is not that surplus lines was used. The trouble is whether the file can support the decision to use it.

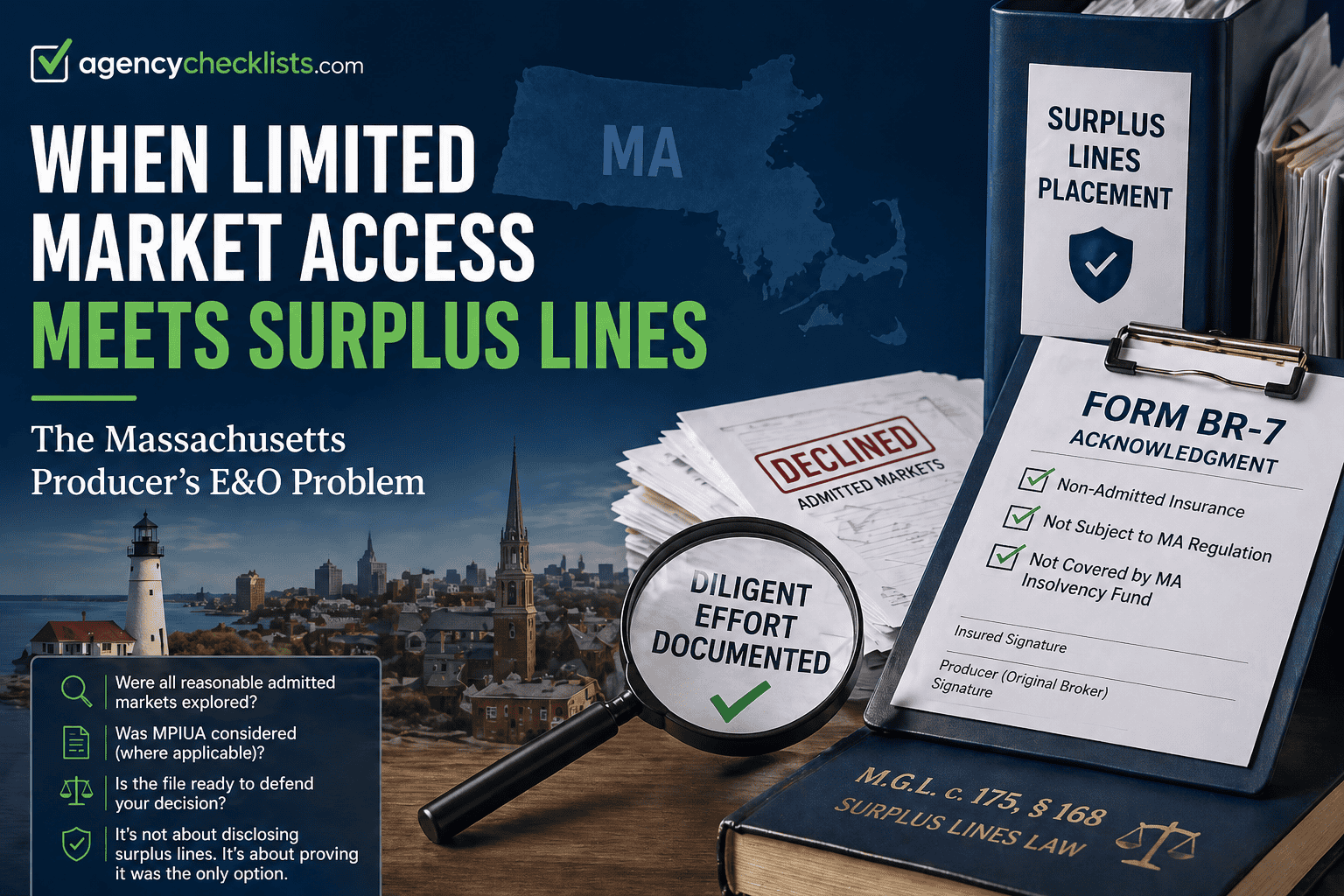

The disclosure issue is largely solved by Form BR-7. The insured acknowledges that the surplus lines insurer is not licensed in Massachusetts, is not subject to Massachusetts regulation, and that losses will not be paid by the state guaranty fund in the event of insolvency. Insolvency is not hypothetical. Reciprocal of America, Vesta, Park Avenue P&C, and a string of program carriers in recent years have all left insureds with unpaid losses. BR-7 puts that risk in front of the insured in writing.

The harder claim is the diligent-effort claim. M.G.L. c. 175, § 168 requires the licensed special insurance broker to file an affidavit stating that the insurance was not procurable, after diligent effort, from admitted Massachusetts companies, and that the surplus lines placement is only the excess over what was procurable from admitted carriers. The retail producer who signs the original-broker portion of BR-7 is putting their name to that representation through the special broker.

If the insured’s expert later identifies an admitted-market channel that was writing similar risks at the time, the producer will be asked what search was actually performed. “We tried our two property markets” is not a defense. “Our agency does not have an appointment with that carrier” is not a defense. The defense is a documented placement process.

What “diligent effort” actually looks like

There is no statutory number of declinations required in Massachusetts. The standard is what a reasonably careful Massachusetts producer would do for that class of business. In practice, that means:

- Markets approached, by name, with dates and underwriter contacts.

- Submissions sent through the agency’s cluster or aggregator (SIAA, Renaissance, Smart Choice, and similar), where applicable, and the responses received.

- Wholesale broker submissions, with the wholesaler’s market summary or quote-and-decline report attached. RPS, AmWINS, Burns & Wilcox, CRC, Bass Underwriters, Specialty Property & Casualty Group of New England, ICW, and the regional houses frequently access admitted markets the retail agency cannot. Their submission summaries are gold-standard documentation.

- For property risks, an MPIUA evaluation.

- For liability risks, an evaluation of class-specific program markets and MGAs.

- A written explanation of why the surplus lines placement was necessary or preferable, with specific reference to coverage differences, capacity, or terms.

Three documented declinations from real admitted markets, plus an MPIUA evaluation, plus a wholesaler decline report, is a defensible file in most circumstances. Two phone calls to two friends at two carriers is not.

A note on the producer’s economic reality. Surplus lines placements typically pay 10 to 12 percent commission, compared to 15 to 20 percent in the admitted market, plus the 4 percent Massachusetts surplus lines tax that the insured pays on top of the premium. Plaintiff’s experts in E&O cases will name those numbers. The defense is a file that shows the producer chose surplus lines because of the risk, not the commission.

MPIUA and Massachusetts property placements

The Massachusetts Property Insurance Underwriting Association, created and governed by M.G.L. c. 175C is the statutory residual market for property insurance. It is admitted, but it is not voluntary admitted capacity, and it occupies a distinct place in the diligent-effort analysis.

The MPIUA producer manual is explicit: an attempt should be made to place coverage in the voluntary insurance market before requesting MPIUA coverage. The manual also confirms that the producer is the agent of the applicant or insured, not of MPIUA or its member companies.

For a Massachusetts property file moving toward surplus lines, the question is not whether MPIUA must be used. The question is whether the producer can explain why MPIUA was unavailable, inadequate, unsuitable, or inferior to the surplus lines policy ultimately recommended. There are good answers for many risks:

- MPIUA’s commercial property forms do not include liability, and many habitational and small commercial accounts need a combined property-and-liability solution.

- MPIUA’s business interruption, theft, and equipment breakdown coverages are limited or unavailable.

- MPIUA personal lines forms are dwelling fire forms, not HO-3 or HO-5, and do not provide the personal liability, contents, and additional living expense protection of a homeowners form.

- MPIUA imposes protective-safeguard requirements, vacancy conditions, and ordinance-or-law sublimits that may not fit the risk.

- MPIUA’s limit caps may be insufficient for the insured’s coverage needs.

Producers should check the current MPIUA producer manual for limit caps and form availability — these have been adjusted in recent years, and any specific number printed in an article will go stale.

The point is not that MPIUA must always be used. The point is that the file should show MPIUA was considered and explain why it was not the answer.

Liability placements and class-specific markets

There is no MPIUA equivalent for most commercial liability risks. The diligent-effort question for liability is whether the producer considered the right class-specific markets.

For most retail producers, that means program markets, MGAs, and admitted specialty carriers reachable through wholesalers — USLI, Markel, Philadelphia, RLI, Distinguished, Hanover Specialty, Berkley specialty units, and class-focused administrators for habitational, hospitality, contractors, trucking, and professional services. Many of these are admitted carriers writing in their specialty class. A producer who never sent the submission to a wholesaler with class expertise has not completed the diligent-effort analysis.

Purchasing groups, risk retention groups, and recognized association programs may also be relevant for some classes. Under M.G.L. c. 176L, a purchasing group is a group formed to purchase liability insurance on a group basis for members with similar liability exposures. The coverage may be written by an admitted insurer, a non-admitted insurer, or an RRG. If admitted, the option is part of the diligent-effort analysis. If non-admitted or through an RRG, the disclosure and guaranty-fund obligations apply: c. 176L confirms that no RRG or its insureds receive Massachusetts insolvency guaranty fund protection, and that purchasing-group coverage from a non-admitted insurer or RRG carries the same gap.

For E&O purposes, the question is not whether the producer searched every purchasing group in the country. The question is whether a reasonably careful Massachusetts producer would have considered a known class-specific program for that class of business before recommending a surplus lines placement.

BR-7 and the original broker’s place in the chain

BR-7 is not paperwork that the wholesaler handles after the fact. It places the original broker squarely in the documentary chain.

The form requires the insured to acknowledge that the broker informed them that the insurance could not be obtained from admitted Massachusetts carriers. The original-broker portion requires the producer to verify that the disclosures were explained and acknowledged. The special broker’s affidavit, signed under penalties of perjury, then states that diligent effort was made — either by the special broker directly or through the retail producer.

Two practical points:

First, BR-7 should be executed contemporaneously with the placement, not retrofitted at audit time. A signature dated months after binding is worse than no signature at all in front of a jury.

Second, BR-7 is not a one-and-done. The diligent-effort analysis applies at every renewal. Admitted-market appetites move. A risk that was unplaceable in the admitted market in 2024 may be placeable in 2026. Each renewal should refresh the file with current declinations and a current MPIUA evaluation, and BR-7 should be re-executed.

The exempt commercial purchaser exception

Section 168 contains an exception that many producers underuse. The affidavit requirement does not apply to an exempt commercial risk or policyholder described in M.G.L. c. 175, § 224 if the commercial risk or policyholder acknowledges in writing that the insurer is not admitted and that, in the event of insolvency, a loss will not be paid by the Massachusetts Insurers Insolvency Fund.

The § 224 thresholds capture more middle-market and larger commercial insureds than producers often assume — measured by net worth, annual revenues, employee count, premium spend, and the sophistication of the risk-management function. For these insureds, the BR-7 process can be replaced with a simpler written acknowledgment, and the placement workflow gets meaningfully cleaner.

The federal Nonadmitted and Reinsurance Reform Act, part of Dodd-Frank, also affects multi-state commercial accounts. It assigns surplus lines tax authority and eligibility analysis to the home state of the insured, which simplifies — and in some cases changes — the analysis for accounts with multi-state exposure.

A producer placing a sophisticated commercial account should know whether their insured qualifies as an exempt commercial purchaser and whether the home-state rule changes the filing posture. Not every account does. But for those that do, the diligent-effort file is replaced by a much shorter document.

Eligible alien unauthorized insurers

M.G.L. c. 175, § 168A governs placements by a special broker with an eligible alien unauthorized insurer. Section 168A does not replace the diligent-effort issue. It permits a special broker licensed under § 168 to procure insurance from an eligible alien unauthorized insurer only if the insurer has been determined by the commissioner to qualify, the special broker files the required affidavit within twenty days, the policy contains the disclosure notice required by § 168, and the other requirements of §§ 168 and 168A are met. The NAIC International Insurers Department list is the practical reference for which alien insurers qualify.

For producers, the practical point is the same: when a Massachusetts risk is placed outside the admitted market, the file should support the conclusion that the required amount or type of insurance was not reasonably procurable from admitted companies after diligent effort.

Coverage differences worth flagging in writing

When a Massachusetts risk moves to surplus lines, the producer’s file should include a written comparison of admitted versus surplus lines coverage on the points that drive losses. The phrases listed below are not jargon — they are the items that turn into denied claims.

- Defense costs: inside or outside the limit of liability.

- Form: special-form versus named-peril.

- Valuation: replacement cost versus actual cash value, with coinsurance terms identified.

- Vacancy provisions: standard vacancy clause, vacancy permit endorsement, or stricter vacancy condition.

- Protective-safeguard endorsements and the consequences of non-compliance.

- Water-damage sublimits and exclusions.

- Ordinance or law: included, sublimited, or excluded.

- Habitational, assault and battery, and abuse exclusions on liability placements.

- Anti-concurrent causation language.

- Claims-made versus occurrence triggers, with retroactive dates.

- Hammer clauses, consent-to-settle provisions, and defense-cost treatment for liability.

A producer who can hand the insured a one-page summary of these points — and retain a signed copy — has gone a long way toward closing the E&O gap that the diligent-effort claim exploits.

A practical file protocol

Before binding a Massachusetts surplus lines placement, the file should answer:

- Which admitted markets did the agency approach, by name and date?

- What did each market say, and was the declination based on the risk, the coverage requested, the limit, the location, prior losses, construction, occupancy, valuation, class code, or appetite?

- Was a wholesale broker engaged, and is the wholesaler’s market summary in the file?

- For property risks, was MPIUA evaluated, and is the reason it was not used documented?

- For liability risks, were class-specific program markets, MGAs, purchasing groups, and risk retention group options considered where appropriate?

- Were coverage differences between the admitted alternative and the surplus lines policy explained in writing to the insured?

- Was BR-7 executed contemporaneously, or, for an exempt commercial purchaser, was the § 224 written acknowledgment obtained?

- Is there a renewal tickler that triggers a fresh diligent-effort analysis at each renewal?

If the file cannot answer these questions, the placement is not finished.

The bottom line on Surplus Lines

Surplus lines is essential infrastructure for Massachusetts property and casualty producers. Coastal three-deckers, older mixed-use buildings, distressed habitational accounts, and high-hazard liability risks are not going away, and the admitted market is not going to write them all.

The E&O risk is not the use of surplus lines. The risk is a file that cannot show why surplus lines was used.

Limited appointments explain why the agency itself could not write the risk. They do not, by themselves, prove that admitted coverage was not reasonably procurable. When a producer signs the original-broker portion of BR-7, the file should show more than a few declined appointments. It should show a documented placement process, a written explanation to the insured, and a reasoned basis — based on the risk and the coverage, not the commission — for concluding that the surplus lines policy was the right answer for the insured the producer was hired to protect.

Owen Gallagher

Insurance Coverage Legal Expert/Co-Founder & Publisher of Agency Checklists

Interested in connecting with me? Call me directly at 617-598-3801.