The Hanover’s Underwriting Performance Improves Across Segments

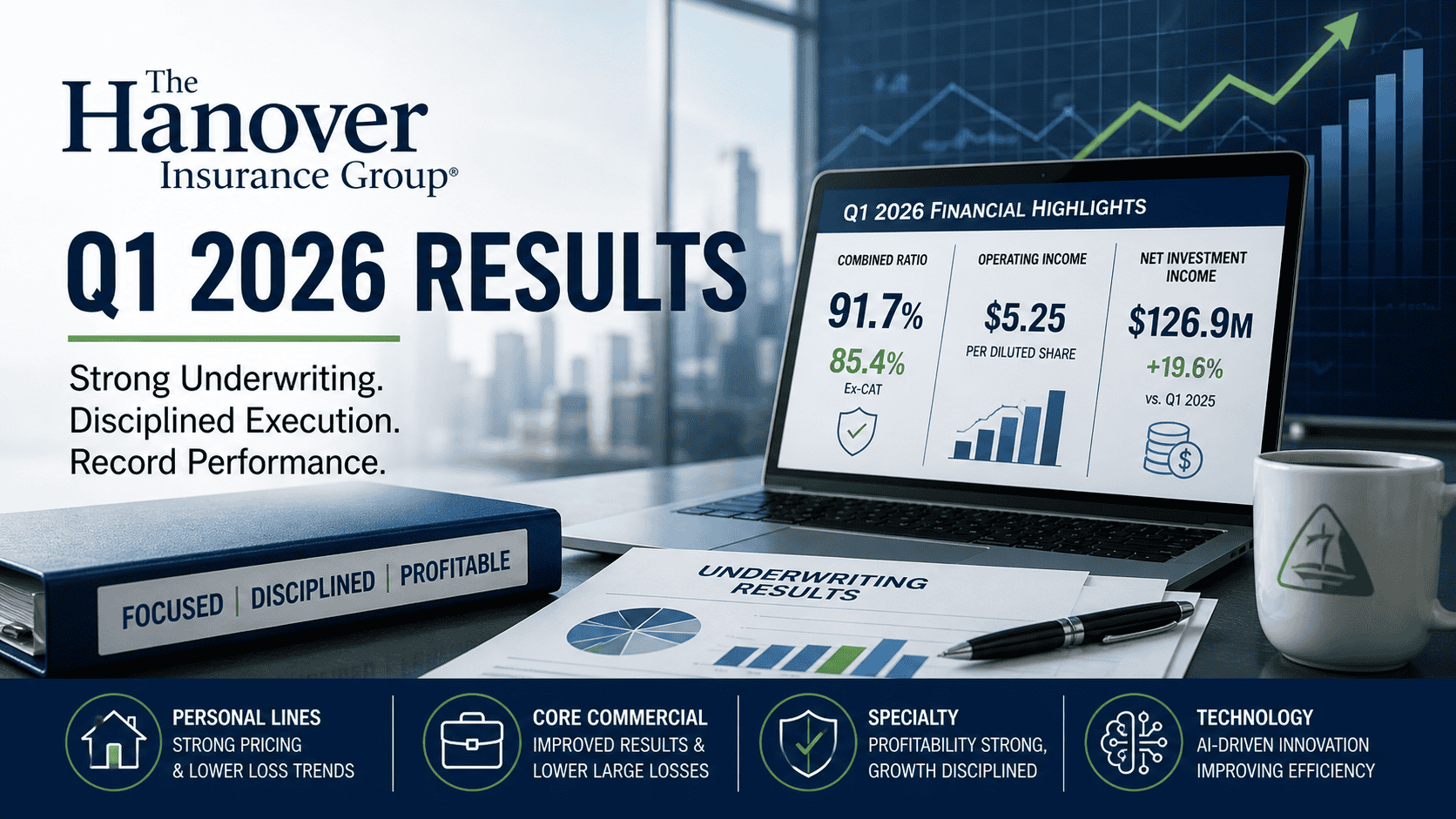

The Hanover Insurance Group reported record first-quarter results for 2026, including operating income of $5.25 per diluted share and a combined ratio of 91.7%, reflecting improved underwriting performance across all segments.

The insurer also reported a combined ratio of 85.4% excluding catastrophes, a 2.4-point improvement from the prior-year quarter, according to its April 29th earnings release.

Chief Executive Officer John C. Roche said the results reflect “disciplined execution” and the impact of prior pricing and underwriting actions.

- Operating income: $5.25 per diluted share (vs. $3.87 in Q1 2025)

- Combined ratio: 91.7% (vs. 94.1%)

- Combined ratio ex-CAT: 85.4% (vs. 87.8%)

- Net investment income: $126.9 million (up 19.6%)

Catastrophe losses accounted for 6.3 points of the combined ratio during the quarter, driven primarily by wind and hail events in the Midwest and winter weather activity, executives said on the earnings call.

The company also reported $25 million of favorable prior-year reserve development, with contributions across all segments.

Personal Lines: Pricing Continues to Outpace Loss Trends

- Net written premiums increased 2.7%

- Current accident year combined ratio (ex-CAT): 83.8%

- Underlying loss ratio improved by 1.1 points

The company reported:

- Homeowners renewal pricing: up 10.8%

- Personal auto pricing: up 6.7%

- Umbrella pricing: up approximately 19%

Executives said earned pricing continues to exceed loss cost trends, with lower claim frequency in property lines contributing to improved results.

Core Commercial: Combined Ratio Improves on Lower Large Losses

- Combined ratio: 96.6% (vs. 103.4% in Q1 2025)

- Current accident year combined ratio (ex-CAT): 91.5%

- Net written premium growth: 4.3%

The improvement was driven in part by lower large property losses compared to the prior-year quarter and continued pricing increases, including average renewal price increases of 8.6%.

Specialty Segment: Profitability Remains Strong as Growth Moderates

- Combined ratio: 84.2% (vs. 87.7%)

- Current accident year combined ratio (ex-CAT): 85.4%

- Net written premium growth: 2.3%

Executives said the company is taking a “measured posture” in property-exposed lines and program business, limiting growth in areas where pricing is under pressure.

During the earnings call, management said it remains “very selective” in program business and distribution relationships, citing competitive conditions in the market.

Technology Initiatives Focus on Underwriting and Claims Efficiency

The company highlighted ongoing investments in technology and artificial intelligence, particularly in underwriting and claims operations.

Executives said the company is deploying AI-enabled tools to:

- Streamline submission intake and triage

- Prioritize underwriting opportunities

- Summarize complex claims and underwriting documents

In the Excess & Surplus business, the company processed approximately 70,000 submissions last year, using new tools designed to improve underwriting efficiency and response times.

Investment Income and Capital Management

Net investment income increased to $126.9 million, driven by higher reinvestment yields and growth in invested assets.

- Book value per share: $101.86 (up 1.0% from year-end 2025)

- Share repurchases: approximately 580,000 shares year-to-date through April 28, totaling about $101 million

The Hanover’s Outlook: Growth Expected to Increase After Q1

Executives indicated that first-quarter premium growth is expected to represent the low point for 2026, with growth anticipated to increase in subsequent quarters.

Roche said the company will continue to focus on underwriting discipline and margin preservation, particularly in lines where pricing conditions are changing.

He added that the company’s strategy remains centered on aligning risk, price, and capital while maintaining its distribution model with independent agents.

Bottom Line for Agents

- Pricing continues to exceed loss trends, particularly in homeowners and umbrella

- Underwriting results improved across all segments, including Core Commercial

- Growth remains measured in competitive or softening markets

- Technology investments are focused on improving underwriting and claims execution

The Hanover’s results reflect continued emphasis on profitability and pricing discipline as market conditions evolve across property and casualty lines.

Previous Quarterly Results for The Hanover

- ‘Record Year Driven by Disciplined Execution’ Says The Hanover’s Roche in Latest Earnings Report

- 3Q-2025: The Hanover Posts A Record 3rd Quarter Based On Good Weather And Pricing

- Q2-2025: The Hanover Posts A Record Q2 Earnings, Citing Pricing Discipline and Strong Underwriting | Agency Checklists

- A Robust Q4 & Full Year 2024 For The Hanover Insurance Group | Agency Checklists