Annual NAMIC-Aon report takes a look at the state of Mutuals each year

With the announcement of the Andover Companies reorganization and the recent significant anniversaries of Massachusetts-based insurers Norfolk & Dedham and Quincy Mutual, Agency Checklists thought it might be interesting to take a look at the state of the Mutual Insurers as a whole. Aiding in this endeavor is an annual report issued by the National Association of Mutual Insurance Companies and Aon. Entitled “The Mutual Factor,” the eighth iteration, published in September of 2025, highlights the impact that mutual insurers have on the insurance industry as a whole.

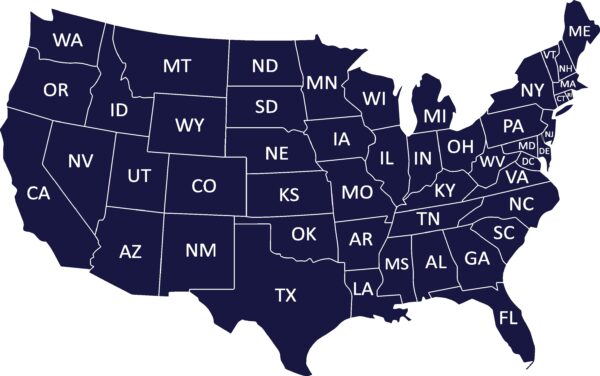

According to the report, mutual insurers accounted for 40% of the U.S. property/casualty market in 2024, compared with 59% for stock insurers and 1% for other segments. In terms of the market share in New England, the mutual segment’s share varied by state, with the following figures cited in the report:

New England Snapshot: Mutual Market Share by State

- Massachusetts: 31%

- Connecticut: 34%

- Rhode Island: 36%

- Vermont: 43%

- New Hampshire: 42%

- Maine: 46%

Nationally, the report notes that mutuals have a consistent presence countrywide: they hold the majority of market share in 12 states and at least 40% in another 23 states, with the strongest mutual presence concentrated in the Midwest. In the four states plus the District of Columbia where mutual market share is below 30%, premiums are typically written by larger national stock insurers such as Allstate, Travelers, Zurich, The Hartford, and Progressive.

Highlights from the Report

The 50 Page Report includes a wide array of information on mutual insurers and how they perform vis-à-vis stock insurers. For example, it notes that mutual insurers and stock insurers posted meaningfully different operating profiles in 2024, even where the headline expense ratios appeared close. The following are some of the metrics included in the report:

Expenses. Mutual insurers reported an expense ratio of 24.7% in 2024, about 0.8 points lower than the 25.5% ratio for stock insurers. The report characterizes this as a year-over-year improvement of about 40 basis points for mutuals, while stock insurers experienced a deterioration of about 70 basis points compared with 2023. Over five years, however, the relationship reverses slightly: mutuals average an expense ratio of 26.0%, about 0.3 points higher than stocks at 25.7%. The total industry is listed at 25.2% for 2024 and 25.9% over five years.

Claims and LAE. The report states mutual insurers typically pay a higher share of each premium dollar in claims and claim-related expenses, including loss adjustment expenses (LAE), than stock insurers. In 2024, mutuals reported a loss and an LAE ratio of 75.5%, compared with 67.9% for stock insurers. On a five-year basis, mutuals are at 77.7% versus 70.3% for stocks. The report highlights that the nearly 7.6-point gap in 2024 is a significant narrowing from 2023, when mutuals reported 84.0% and stock insurers 71.1%—a difference of about 13 points. Total-industry loss and LAE ratios are cited as 71.0% in 2024 and 73.4% over five years.

Commissions and servicing costs. Mutuals show a materially lower net commission ratio than stock insurers. In 2024, mutuals reported 9.1%, compared with 11.8% for stocks; over five years, mutuals are at 9.3% versus 12.1% for stocks. The report attributes this advantage to how business mix and distribution type can affect commission structures for large mutual insurers. By contrast, direct general expenses are nearly identical: 5.5% for mutuals and 5.4% for stocks in 2024, and 5.7% versus 5.6% over five years.

Dividends. The report emphasizes that policyholder dividends are far more common among mutuals, reflecting that policyholders are also owners. In 2024, mutuals paid dividends equal to 0.9% of net premiums, compared with 0.1% for stock insurers (total industry 0.5%). Over five years, mutuals average 1.2%, while stocks remain at 0.1%. The report notes the mutual dividend ratio declined in 2024 compared with the recent five-year period as companies return to underwriting profitability, while describing dividends as a retention tool and a reward for low-claim policyholders.

AM Best Rating Methodology

The NAMIC–Aon report also includes a “Benchmark Study for AM Best Ratings” to compare mutual and stock property/casualty insurers. The comparison, conducted under Best’s Credit Rating Methodology, is a framework that combines quantitative and qualitative measures and is maintained through a continuous dialogue between AM Best analysts and company management. The benchmark study covers 595 U.S. P&C insurers (groups and unaffiliated single companies) rated as of July 16, 2025, with the report classifying the sample as 55% stock and 45% mutual; it also notes that stock companies within mutual group ratings were counted as a single mutual company, and that reciprocal exchanges, risk retention groups, cooperatives, and Lloyds were counted as mutual companies.

Within that dataset, the report’s key findings in its benchmark study indicate that mutuals score strongly on several AM Best measures. It reports the following:

- 86% of mutual companies are rated “A-” or higher, and 84% have a “Positive” or “Stable” outlook. Mutuals also post a higher median VaR 99.6 BCAR score at 53%, compared with 46% for stock companies.

- On balance sheet strength, 88% of mutuals are assessed as “Strongest” or “Very Strong,” compared with 80% of stock insurers.

- The report shows mutuals slightly behind stocks in operating performance distribution, with 85% of mutuals receiving “Adequate” or better assessments compared with 90% for stocks, and also states that stocks exhibit 17% higher combined-ratio volatility (standard deviation) than mutuals on a median five-year basis.

- It also finds 47% of mutuals have a “Neutral” or better business profile, compared with 40% of stocks, and 96% of mutuals have an “Appropriate” or better ERM assessment, versus 94% for stock insurers.

- Finally, the report distinguishes between external support, stating that only 4% of mutuals receive a rating lift from parent affiliation, compared with 23% of stock companies that depend on such a lift.

In the rating distribution itself, the report says most of the 595 companies are rated either “A” or “A-.” It notes that slightly fewer mutuals sit at the very top of the scale—9% of mutuals are rated “A++/A+,” compared with 11% of stock companies—while a larger share of mutuals received an “A” rating (46% for mutuals versus 34% for stocks, as cited for 2023). At the lower end, the report states 7% of stock companies were rated “B+” or lower, compared with 4% of mutuals.

Market Share Data

For readers interested in the largest mutual insurers in the nation, the report also provides market share data on the top mutual insurers in the United States across various lines of insurance.

How to access a copy

The report is free on the NAMIC website. A copy can be accessed via this link.