AG Alleges Years-Long Scheme Misled Consumers on Nature of Coverage

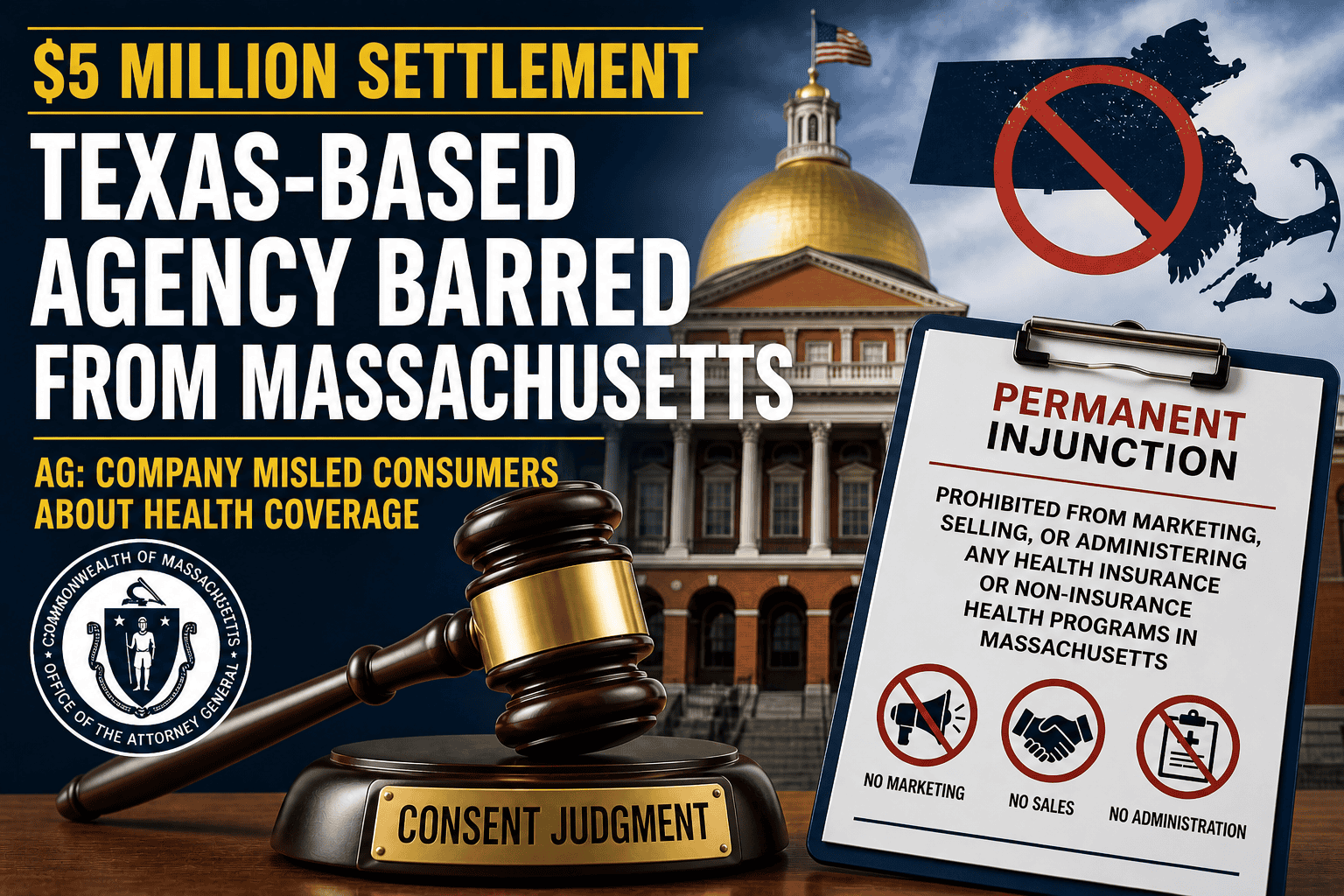

A Texas-based health insurance agency has been permanently barred from operating in Massachusetts and will pay $5 million to resolve allegations that it systematically misled consumers into buying health plans that did not provide the coverage they believed they were purchasing.

The consent judgment, entered April 29, 2026, in Suffolk Superior Court, concludes a multi-year investigation by the Massachusetts Attorney General’s Office into Adroit Health Group LLC, The Adroit Group, LLC, and A1 Health Group, LLC (collectively, “Adroit”).

Attorney General Andrea Joy Campbell said the company sold products to Massachusetts residents “as comprehensive health insurance plans that met federal and state requirements, when in fact the company did not sell qualifying insurance plans.”

$5 Million Settlement Structured Over Three Years

Under the Final Judgment by Consent, Adroit will pay $5 million in staged payments through 2028, including:

- $2.0 million for restitution to affected Massachusetts consumers

- $1.5 million additional restitution by March 15, 2027

- $1.5 million by March 15, 2028, including:

- $500,000 for restitution

- $800,000 in civil penalties

- $200,000 for investigation costs

The Attorney General’s Office will oversee the distribution of restitution funds to impacted consumers.

The judgment was entered without an admission of liability by Adroit.

Permanent Ban From Massachusetts Market

The court order imposes a permanent injunction prohibiting Adroit and its affiliates, successors, and agents from:

- Marketing or selling any health insurance policy

- Offering or administering any non-insurance health program

- Conducting such activities for Massachusetts residents

The prohibition extends to any future business entities or operating names used to reach Massachusetts consumers.

Complaint Details Widespread Misrepresentation of Coverage

The Attorney General’s complaint alleges that Adroit built its business by presenting limited-benefit products and discount programs as comprehensive health insurance.

According to the complaint:

- Consumers were told they were purchasing plans comparable to major medical coverage

- Sales agents used insurance terminology such as “PPO” and “coverage” to describe non-insurance products

- Consumers were led to believe the plans satisfied the Affordable Care Act (ACA) and Massachusetts’ Minimum Creditable Coverage (MCC) standards when they did not

The complaint alleges that, in reality, the products included:

- Discount health plans that only reduced the cost of services

- Limited-benefit policies with significant coverage gaps

- Health care sharing arrangements that did not guarantee payment of claims

Billing and Cancellation Practices at Issue

Beyond the initial sale, the complaint alleges that Adroit’s business practices continued to disadvantage consumers after enrollment.

Among the allegations:

- Consumers were charged without authorization, including instances where no signed agreement existed

- Cancellation requests were not processed, including those submitted by email

- Consumers were routed back to the same sales agents who had enrolled them when attempting to cancel

- Refunds were withheld, including during advertised “free-look” periods

The complaint also alleges that some consumers continued to be billed after attempting to cancel and were left with significant out-of-pocket medical costs for services they believed were covered.

Use of Multiple Business Names and Lead Generation Tactics

The Attorney General further alleged that Adroit operated under multiple names, including “Strata Health Group” and “A1,” and used lead-generation websites designed to resemble official or government-sponsored enrollment platforms.

According to the complaint, these practices contributed to consumer confusion about the nature of the products being sold and the entity responsible for the coverage.

Scope and Timeline of Conduct

According to the filings:

- Adroit began marketing these products to Massachusetts consumers in 2016

- The company represented that it stopped selling plans to new Massachusetts customers by approximately January 2022

The Attorney General’s Office alleged that the conduct affected thousands of Massachusetts consumers over that period.

Regulatory Framework

The Commonwealth brought its claims under:

- The Massachusetts Consumer Protection Act, G.L. c. 93A

- Insurance marketing and disclosure regulations under 211 CMR 40.00

- Specified disease insurance regulations under 211 CMR 146.00

The consent judgment resolves those claims without trial.

Takeaways for Insurance Professionals

For Massachusetts, the case highlights the Attorney General’s continued regulatory focus on:

- The marketing of supplemental and limited-benefit products

- Clear disclosure of the distinction between insurance and non-insurance programs

- Oversight of third-party entities controlling enrollment, billing, and consumer communications

The enforcement action underscores that liability exposure in Massachusetts extends beyond underwriting to the full distribution chain, particularly where consumer-facing representations are at issue.

Attorney General’s Team

The matter was handled by Deputy Division Chief Ethan Marks, Assistant Attorney General Nina Cohen, Senior Enforcement Counsel Emiliano Mazlen, and Paralegal Gaëlle Bouaziz of the Attorney General’s Health Care Division, with assistance from Senior Investigator Anthony Crespi of the Civil Investigations Division.