A new class action suit is filed in Massachusetts

Notwithstanding the adamant position of insurers that there is no coverage for business interruption claims arising out of the COVID-19 shutdowns, insureds are not all taking that “No” as the final answer. As Agency Checklists previously reported, the Legal Sea Food chain sued the Greater New York Mutual Group for the denial of Legal’s business interruption claim. See Agency Checklists’ article of May 12, 2020, “Legal Sea Foods Files A COVID-19 Business Interruption Coverage Suit Against Strathmore Insurance.”

Also, the Massachusetts Legislature still has before it a bill, applicable to in-force policies, that prohibits any insurer from denying a claim:

“for the loss of use and occupancy and business interruption on account of (i) COVID-19 being a virus (even if the relevant insurance policy excludes losses resulting from viruses); or (ii) there being no physical damage to the property of the insured or any other relevant property.”

–See Agency Checklists’ article of “April 14, 2020, “Will Insurers Be Required To Pay COVID-19 Business Interruption Claims?”

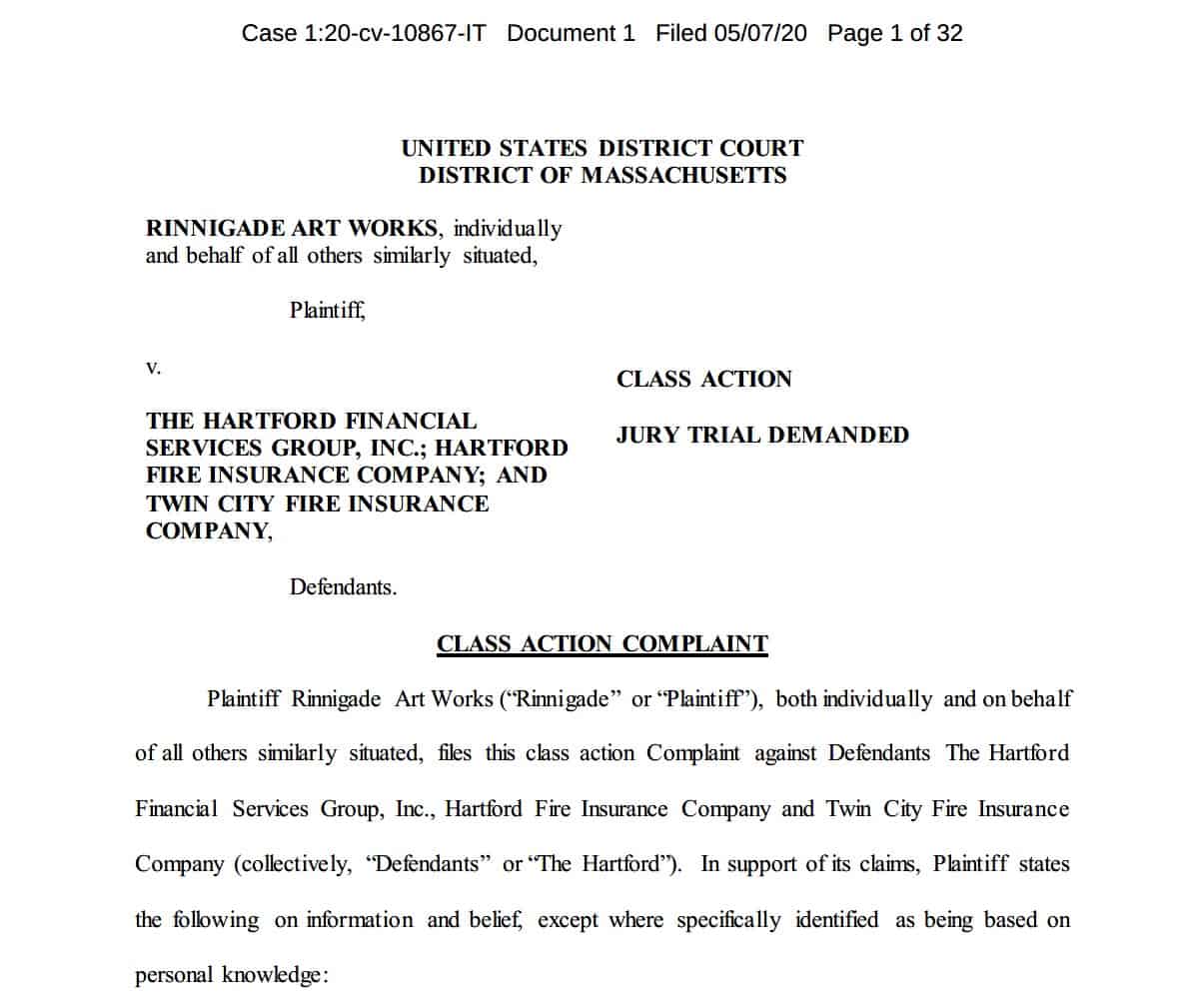

A Somerville-based business has filed the class-action suit against The Hartford

Now a small Somerville business, Rinnigade Art Works, LLC, a graphic art and design company, has filed a class-action suit against The Hartford Financial Services Group, Inc., and two of its subsidiary insurers, the Hartford Fire Insurance Company and the Twin City Fire Insurance Company (“The Hartford”).

The complaint alleges that The Hartford improperly denied coverage to Rinnigade and other commercial insureds for lost business income and extra expenses resulting from the COVID-19 pandemic and action of civil authorities in ordering the closure of business locations.

The nine counts in Rinnigade’s complaint as filed alleged breach of contract and sought declaratory judgments for designated classes (as defined below) as well as a count under G.L. c. 93A, §§ 2 and 11 alleging unfair claim practice under c. 176D § 9(3).

The Rinnigade Spectrum business owner’s policy

The Twin City Fire Insurance Company was the only insurer issuing coverage to Rinnigade. The 162-page business owner’s policy had effective dates between February 25, 2020, and February 25, 2021.

The property portion of the policy provided $628,000 in replacement cost for business personal property but no building coverage. The policy also provided business income and extra expense, action of civil authority, extended business income, and business income from dependent property coverages. The liability portion provided a $1,000,000 bodily injury and personal injury limit. The premium for the total package of coverages offered by the policy totaled $2,879.

While the policy had various endorsements and exclusions, it had no specific virus pandemic exclusion. However, all the business interruption related coverages did require as a condition precedent for coverage “direct physical loss or damage.”

The March 23, 2020 COVID-19 Order as supposedly causing direct physical loss or damage

In its fact section, the complaint outlines the progression of the public health emergency in response to the appearance of the novel coronavirus in Massachusetts. In particular, the complaint identifies the March 23, 2020 COVID- 19 Order No. 13, issued by Governor Baker. This order required all businesses and organizations that did not provide COVID- 19 essential services to close their physical workplaces and facilities to workers, customers, and the public. Also, the order prohibited any businesses that offered food and beverage products to the public from allowing on-premises consumption.

The complaint alleges that as a result of these “facts and circumstances” Rinnigade had “direct physical loss or damage to property at the premises covered under the Policy” including:

- The property being damaged,

- Access to the property being denied,

- Customers being prevented from physically occupying the property,

- The property being physically uninhabitable by customers,

- The function of the property being nearly eliminated or destroyed

- A suspension of business operations occurring at the property, and,

- Plaintiff has only been able to operate on a limited basis.

The complaint also alleged that Rinnigade sustained business income losses due to direct physical loss or physical damage at the premises of dependent properties.

Denial of coverage by The Hartford for no direct physical loss or damage

Sometime in early April, Rinnigade furnished The Hartford notice under the policy of its ongoing business interruption related damages. On April 15, 2020, The Hartford denied Rinnigade’s claim based upon none of its business interruption related claims having resulted from direct physical loss or damage.

In its complaint, Rinnigade claims that its policy does not have any exclusion that allowed The Hartford to deny Rinnigade’s claim for its business interruption and action of civil authorities losses payable under the policy.

As stated in its complaint, Rinnigade’s position is that “because the policy is an all-risk policy and does not specifically exclude the losses that [Rinnigade] has suffered, those losses are covered.”

The suit seeks class-action status

In filing its suit, Rinnigade seeks to have the suit certified as a class action. Besides the question of liability, Rinnigade will have to satisfy to the Court that allowing the lawsuit to proceed on a class basis; the following conditions have been met:

Class number. There must be enough potential other plaintiffs to establish a class with sufficient numerosity. Rinnigade will have to find out at least the approximate number of Massachusetts commercial insureds denied COVID-19 business interruption insurance coverage by The Hartford.

Common issues. Rinnigade must show it has common questions of law or fact with the other proposed business interruption class members. E.g. Are all The Hartford’s commercial property policies issued with uniform terms and conditions like Rinnigade’s?

Typicality. Rinnigade’s business interruption insurance claims must be typical of the claims of the other proposed business interruption class members.

Adequacy. Rinnigade, as the class representative, must adequately represent the interests of the class, and Rinnigade’s counsel must be competent and experienced in class actions.

Predominance of common issues. The class members cannot have individual fact-specific claims that overshadow the common issues. The common legal issues must predominate.

Superiority of class proceedings. The Court has to find that a class action joining all the COVID-19 business interruption related claims would be superior to allowing individual actions by each insured.

If Rinnigade meets these class conditions, his complaint seeks an order from the Court certifying four classes of insureds and one subclass. The four putative classes of insureds consist of:

- The Business Income Coverage Class.

- The Extra Expense Coverage Class.

- The Business Income from Dependent Properties Coverage Class; and,

- The Civil Authority Coverage Class.

These four proposed classes each consist of:

“All persons and entities with [the specified type of] coverage under a property insurance policy issued by [The Hartford] that suffered a suspension of business operations and for which [The Hartford] has either actually denied or stated it will deny a claim for the losses or have otherwise failed to acknowledge, accept as a covered loss, or pay for the covered losses.”

The fifth class, designated as the “Massachusetts Subclass” would consist of “All persons and entities within the Business Income Class, the Extra Expense Coverage Class, the Business Income from Dependent Properties Coverage Class or the Civil Authority Coverage Class engaged in the conduct of trade or commerce in the Commonwealth of Massachusetts. The technical term “engaged in the conduct of trade or commerce in the Commonwealth” derives from G.L. c. 93A and states the requirement for seeking multiple damages and attorney fees for unfair claim practices or acts.

Agency Checklists will keep you posted

Since Rinnigade only filed its complaint on May 7, 2020, The Hartford has not yet had an opportunity to respond by way of an answer, a motion to dismiss, or for judgment on the pleadings.

Agency Checklists will monitor this case as it progresses and keeps its readers posted as to any further developments.

Owen Gallagher

Co-Founder & Publisher Agency Checklists

Owen is an experienced insurance litigator as well as a certified mediator and arbitrator who specializes in insurance industry disputes. His interest and affinity for insurance began at a young age working the counter at his father’s assigned risk agency in Roxbury.

Over the course of his career, Owen has argued a number of cases in the Massachusetts Supreme Judicial Court and has helped agents, insurance companies, and lawmakers alike with the complexities and idiosyncrasies of insurance law in the Commonwealth. Contact Owen via one of the links below: