Taxiway Defect Causes a $1.45 Million Aircraft Damage Claim

A small defect in a stretch of airport pavement—something that might barely register in most commercial settings—set off a chain of events that has now produced a federal court ruling on the limits of Commercial General Liability coverage and a reminder of how much can turn on a few lines of policy language.

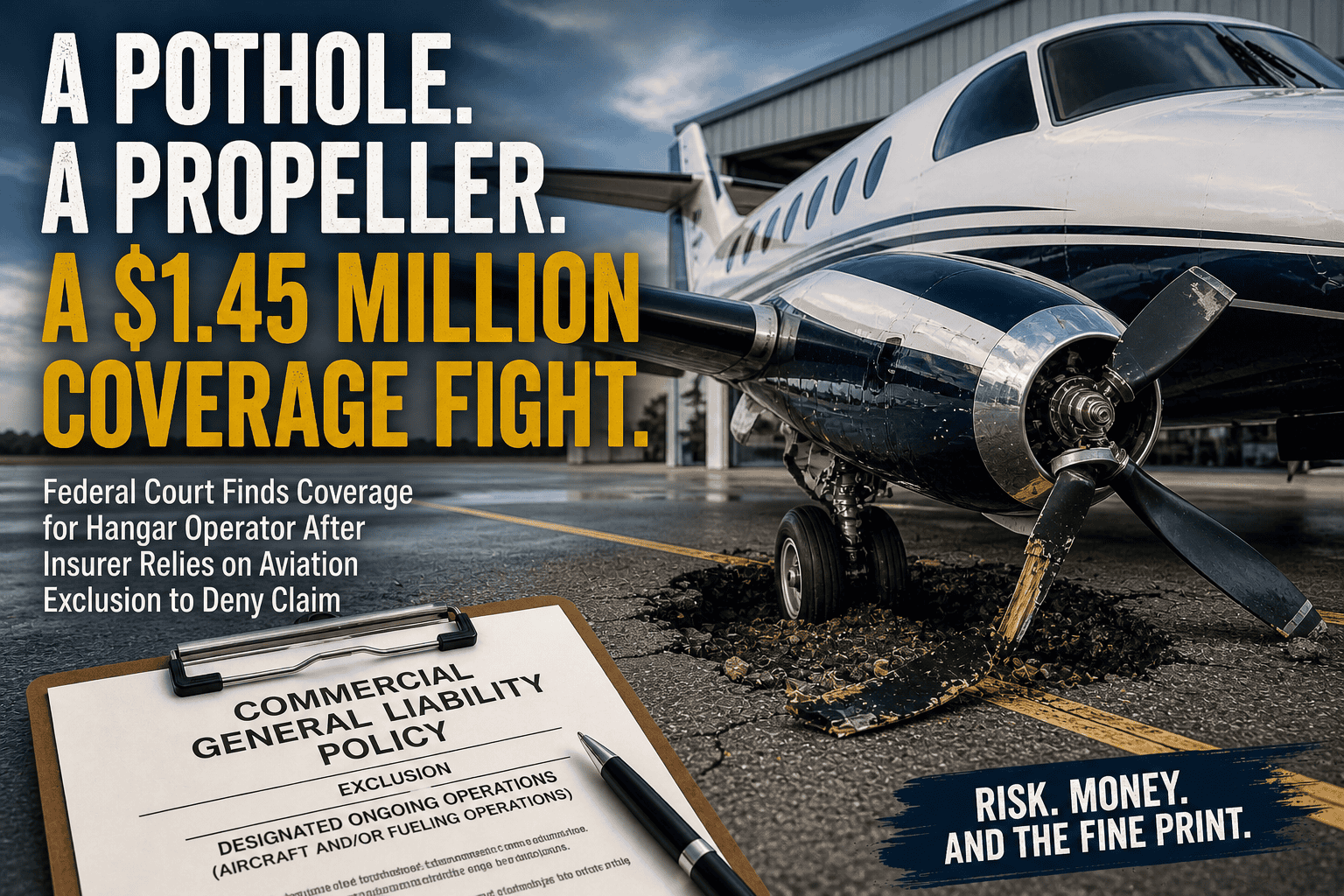

The case, Vineyard Aircraft Hangars Inc. v. New Hampshire Insurance Company, arises from a February 2022 incident at Martha’s Vineyard Airport. A pilot taxiing a six-passenger 2021 turboprop aircraft out of a hangar operated by Vineyard Aircraft Hangars Inc.(“MAH”) hit what the underlying complaint describes as a pothole or sinkhole in the apron. The front wheel dropped, the propeller struck the pavement, and what followed was not just a repair job, but a cascading financial loss typical of aviation claims.

By the time the owner of the aircraft, Suite Six LLC, filed suit, its claim had climbed to at least $1.45 million. Roughly $289,000 was attributed to physical repairs. Another $71,000 was claimed for loss of use and related losses. The largest component—nearly $868,000—was for diminution in the aircraft’s value, reflecting the well-known market stigma attached to a “prop strike.” An additional $225,000 was tied to increased insurance premiums.

A Premises Liability Case—Not an Aviation Operations Claim

The aircraft owner’s federal lawsuit that followed did not accuse the hangar operator of anything involving the operation of aircraft. Instead, it sounded in familiar premises liability terms: failure to maintain the apron, failure to address hazardous conditions, and breach of an agreement to keep the surface safe for aircraft access.

That framing would prove decisive.

Vineyard Aircraft Hangars tendered the claim to its insurer, New Hampshire Insurance Company. The response was swift. Within days, the insurer denied coverage outright.

The Fine Print: When “Aircraft Operations” Meets Premises Risk

The denial relied on a “Designated Ongoing Operations” exclusion appended to the policy. That endorsement identified “Aircraft and/or Fueling Operations” as excluded risks and stated that the exclusion applied “regardless of whether such operations are conducted by you or on your behalf or…for others.”

From the insurer’s perspective, the analysis was simple: the aircraft was in motion when the loss occurred, so the damage arose out of aircraft operations. It should not matter who was operating the aircraft.

The insured saw the policy through a different lens. Vineyard Aircraft Hangars is not in the business of flying or fueling aircraft; it operates hangar space and the surrounding premises. Its risk exposure lies in the condition of the ground, not the operation of planes. To read the exclusion as applying to any incident involving a moving aircraft, the company argued, would be to strip the policy of coverage for the risks inherent in its business.

The Court Finds Ambiguity—and a Coverage Obligation

After a round of demand and denial letters, back and forth, MAH filed a declaratory judgment against New Hampshire Insurance in Boston’s federal court, where the aircraft owner’s suit pended.

On cross-motions for summary judgment, federal judge Angel Kelley approached the dispute using settled Massachusetts principles: Policy language is read in its ordinary sense, exclusions are construed narrowly, and ambiguities are resolved in favor of the insured.

The policy did not yield a clean answer. Alongside the specialized “Designated Ongoing Operations” exclusion sat a more conventional aircraft exclusion, one that barred coverage for aircraft owned or operated by the insured. The interaction between those provisions created an interpretive problem neither side could fully resolve.

The court focused on the wording of the endorsement itself. The phrase “regardless of whether” could plausibly be read broadly, as the insurer urged, or more narrowly, as referring back to the insured’s own operations. Because both interpretations were reasonable, the court found the exclusion ambiguous.

That ambiguity mattered. The court declined to adopt an interpretation that would effectively eliminate coverage for a hangar operator whenever an aircraft was moving on its premises—an everyday and unavoidable condition of its business.

The underlying complaint, grounded in negligent maintenance of the apron, was at least reasonably susceptible to coverage. That was sufficient to trigger the duty to defend. But the ruling did not stop there. The court granted declaratory relief and found that the insurer had breached its contract, requiring it to respond under the policy’s terms, including indemnity.

The Chapter 93A Claim: Why the Insurer Avoided Bad Faith Liability

Although the insurer lost on coverage, it prevailed on the insured’s claim under M.G.L. c. 93A.

For Massachusetts insurance professionals, that portion of the decision is as instructive as the coverage ruling itself.

The insured argued that the denial was not just incorrect, but unreasonable—an attempt to stretch policy language beyond any plausible meaning. The court disagreed. It characterized the dispute as a conventional disagreement over contract interpretation, not an unfair or deceptive act.

The key distinction is a familiar one under Massachusetts law: an incorrect coverage position is not, by itself, a violation of Chapter 93A.

To impose liability, courts typically look for a lack of any reasonable basis for the denial, conduct reflecting bad faith or coercion, or a failure to engage with the claim in a fair and reasoned way. Here, the insurer’s reading of the exclusion—while ultimately unsuccessful—was grounded in the text of the endorsement and supported by legal argument. That was enough to qualify as a plausible, reasoned position.

As a result, the court treated the matter as an ordinary contract dispute, not an unfair claims practice.

For carriers, the takeaway is straightforward: a defensible legal interpretation, even if rejected, can insulate against 93A exposure. For insureds, it underscores the higher threshold for converting a coverage dispute into a bad faith claim.

The Strategic Risk: Denying a Defense Outright

The more consequential risk for the insurer lay not in 93A exposure, but in its decision to deny a defense outright.

Massachusetts practice gives carriers a well-established alternative: defend under a reservation of rights while litigating coverage. That approach preserves the insurer’s position without forfeiting control of the defense or exposing it to additional cost consequences.

Here, the insurer chose a different path. It denied the defense at the outset.

That decision carried consequences once the court found a duty to defend and indemnify. The insurer now faces exposure not only for the defense costs incurred in the underlying action and any indemnity owed under the policy, but also for the insured’s legal fees incurred in establishing its right to a defense.

That last category—coverage counsel fees—can materially increase the cost of a denial, particularly in a case of this size.

What Comes Next: The Unresolved Question of Diminished Value

The ruling resolves the insurer’s obligation to respond under the policy, but it does not end the story.

The largest component of the claimed damages—nearly $868,000—relates to diminution in value. In aviation, a propeller strike can permanently affect an aircraft’s resale value, even after repairs are completed.

Massachusetts courts have addressed similar issues in the automobile context, where claims for inherent diminished value have been litigated under property damage provisions. Whether those principles will carry over in this setting remains an open question as the underlying case proceeds.

A Familiar Coverage Lesson in an Unusual Setting

At its core, the case reflects a familiar dynamic in liability insurance. Insurers draft exclusions to limit exposure. Insureds purchase coverage expecting protection against the ordinary risks of their operations. When those expectations diverge, the outcome often turns on how precisely the policy language has been written—and how narrowly a court is willing to read it.

Here, the dispute began with a pothole and a damaged propeller. It turned into a seven-figure claim and a close reading of a single endorsement. And it ends, for now, with a reminder that in Massachusetts, ambiguity in the fine print is likely to be resolved in favor of coverage—even as the bar for bad faith remains considerably higher.

Other insurance coverage case analysis by Agency Checklists

- No Chapter 93A Liability When Insurers Refuse Additional Insured Coverage to Each Other’s Insureds

- Court Rules Liability Insurer Can Recover Defense Costs & $1.5 Million Settlement from Insured

- Massachusetts Court Rules On Liability Insurer Summarily Denying Chelsea Condo Coverage Based On A Complaint Alone

Owen Gallagher

Insurance Coverage Legal Expert/Co-Founder & Publisher of Agency Checklists

Interested in contacting me? Call me directly at 617-598-3801.